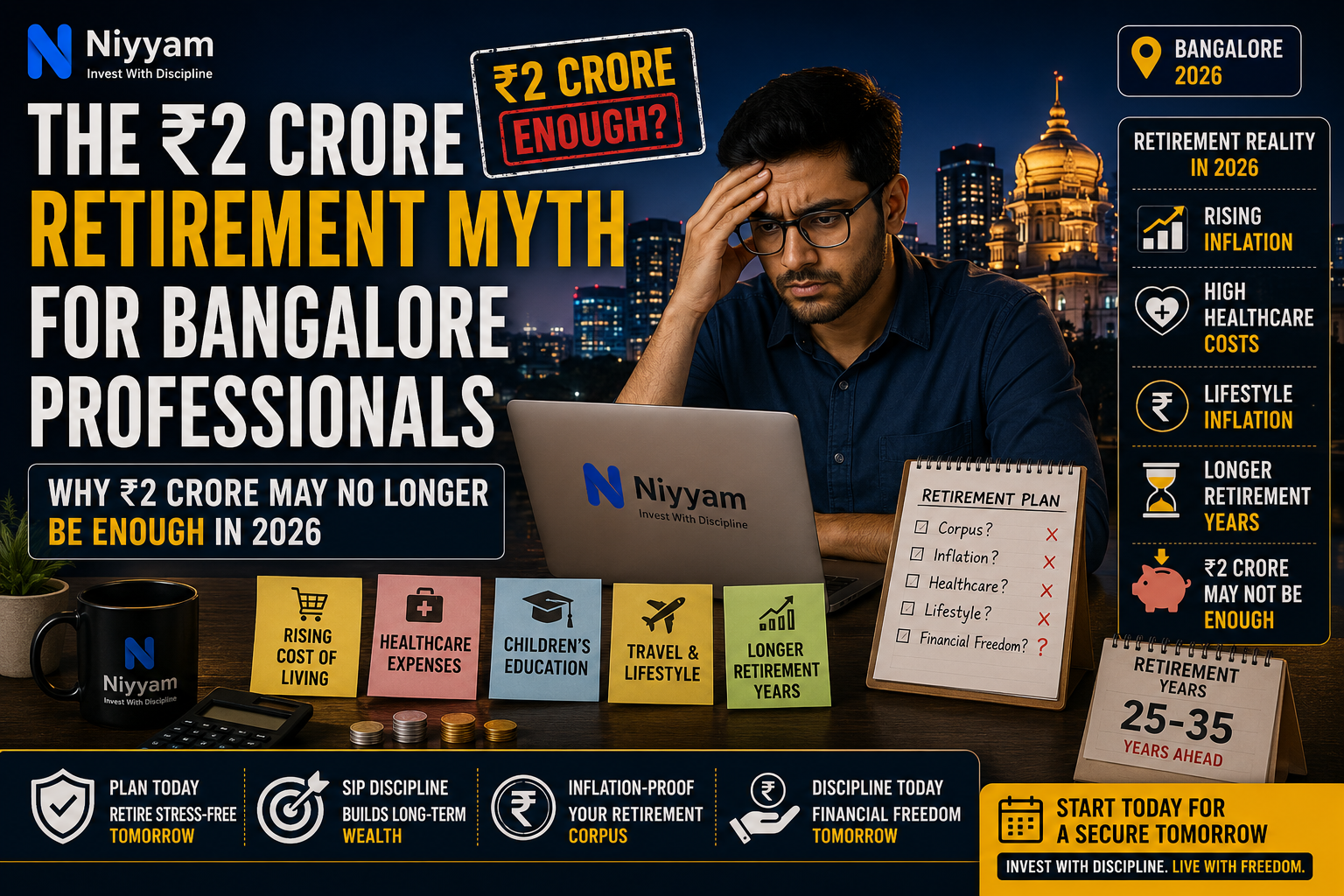

Why ₹2 Crore May No Longer Be Enough for Retirement in 2026

By Ashok Prasad, Founder, Niyyam

Published: May 2026

Introduction

The ₹2 Crore Retirement Myth is becoming one of the biggest financial concerns among Bangalore professionals in 2026. Rising inflation, healthcare costs, lifestyle inflation, and longer retirement periods are forcing salaried professionals to rethink whether ₹2 crore is truly enough for long-term financial security.

For a long time, ₹2 crore sounded enormous.

People imagined:

- a stress-free retirement,

- complete financial independence,

- stable monthly income,

- comfortable healthcare,

- and lifelong peace of mind.

But Bangalore’s financial reality in 2026 is changing rapidly.

Today:

- inflation is rising aggressively,

- healthcare costs are exploding,

- urban lifestyles are becoming more expensive,

- and retirement periods are becoming significantly longer.

As a result:

₹2 crore may no longer provide the retirement comfort many professionals imagine.

This is especially true for:

- Bangalore tech employees,

- salaried middle-class families,

- and urban professionals are accustomed to modern city lifestyles.

And this is exactly why retirement planning is becoming one of the most important financial discussions in India today.

💡 Key Takeaways

- ₹2 crore is NOT automatically enough for retirement in Bangalore anymore.

- Inflation quietly destroys long-term purchasing power.

- Healthcare costs are rising faster than many people expect.

- High salary does NOT guarantee retirement security.

- Lifestyle inflation is one of the biggest retirement threats today.

- Retirement planning is no longer about one fixed number.

- Disciplined SIP investing and long-term financial behavior matter far more than chasing random retirement targets.

- Starting retirement investing early is becoming critically important.

Direct Answer

Is ₹2 Crore Enough for Retirement for Bangalore Professionals in 2026?

For many urban professionals in Bangalore:

The answer is probably NO.

Not because ₹2 crore is a small amount.

But because:

- inflation reduces future purchasing power,

- healthcare expenses are rising rapidly,

- retirement periods are becoming longer,

- and urban lifestyles have become significantly more expensive.

For many Bangalore families,

₹2 crore may provide:

- partial retirement support,

- moderate financial stability,

- or basic retirement comfort.

But it may NOT guarantee:

long-term financial freedom for 25–35 years after retirement.

Especially for professionals used to:

- premium healthcare,

- urban living,

- travel,

- comfortable lifestyles,

- and rising monthly expenses.

Why ₹2 Crore Feels Like a Huge Amount

Psychologically,

₹2 crore still feels massive because many professionals grew up in an India where:

- ₹1 lakh salary was considered extraordinary,

- apartments cost ₹20–30 lakhs,

- healthcare was affordable,

- and retirement expenses were significantly lower.

But Bangalore in 2026 is completely different.

Today:

- premium apartments cost crores,

- Medical expenses are rising sharply,

- Private education is expensive,

- And even middle-class urban living requires substantial monthly spending.

This means:

Retirement calculations made 10–15 years ago may no longer work today.

Inflation Is the Biggest Retirement Threat

The single biggest retirement risk is:

Inflation

Most people underestimate how dangerous long-term inflation can become.

Even if inflation averages:

- 6–7% annually,

The cost of living can double approximately every 10–12 years.

That means:

- groceries,

- rent,

- domestic help,

- transportation,

- utilities,

- healthcare,

- insurance,

- and daily lifestyle expenses

may all become dramatically more expensive in the future.

Example: Bangalore Retirement Reality

Suppose a Bangalore family needs:

- ₹1 lakh per month today

for a comfortable urban lifestyle.

After 20 years of inflation,

that same lifestyle may require:

- ₹3–4 lakhs per month or even more.

Now think about this carefully.

A retirement corpus that feels “large” today may feel surprisingly inadequate later.

This is why:

Retirement planning must focus on future purchasing power — not today’s money value.

Healthcare Costs Are Becoming Dangerous

One of the biggest retirement problems today is:

Healthcare Inflation

In Bangalore:

- hospitalization costs are increasing rapidly,

- premium healthcare is becoming expensive,

- and medical emergencies can wipe out retirement savings quickly.

A single major medical issue after retirement can create enormous financial pressure.

This becomes even more dangerous because:

- people are living longer,

- lifestyle diseases are increasing,

- and healthcare costs usually rise faster than normal inflation.

Many retirees underestimate:

- ICU costs,

- long-term medication expenses,

- scans and diagnostics,

- home healthcare,

- and elderly dependency costs.

This is why retirement planning today is NOT only about savings.

It is also about:

financial protection and long-term stability.

Lifestyle Inflation Quietly Destroys Retirement Planning

One of the biggest financial misconceptions is:

“Expenses will automatically reduce after retirement.”

But for many Bangalore professionals,

that may not happen.

Today’s urban professionals are already accustomed to:

- air-conditioned lifestyles,

- premium apartments,

- eating out,

- subscriptions,

- gadgets,

- vacations,

- and convenience-based living.

These habits rarely disappear completely after retirement.

In many cases:

People actually want MORE comfort after retirement.

And this creates a serious long-term financial challenge.

This is exactly why Your Salary Increased… But So Did Your Expenses became highly relatable for Bangalore professionals.

Because:

High income does NOT automatically create wealth.

Longer Life Expectancy Changes Everything

Earlier generations often retired at:

- 58–60,

and had relatively shorter retirement periods.

But today,

many professionals may spend:

25–35 years in retirement.

This completely changes retirement mathematics.

Your retirement corpus must survive:

- inflation,

- healthcare,

- emergencies,

- and lifestyle expenses

for potentially three decades or more.

This is why:

Retirement planning is becoming far more complex than simply targeting ₹2 crore.

Why High Salary Professionals Still Feel Financially Insecure

Interestingly,

many professionals earn:

- ₹20 LPA,

- ₹40 LPA,

- or even higher salaries

still feel financially stressed.

Why?

Because:

High income does NOT automatically create financial freedom.

Many people struggle with:

- high EMIs,

- weak investing discipline,

- inconsistent SIP investing,

- lifestyle inflation,

- and poor long-term financial planning.

This is exactly why The Silent Financial Stress Nobody Talks About in Bangalore’s Tech Industry became an important discussion among salaried professionals.

Because many people appear financially successful externally —

while internally feeling financially insecure.

The Retirement Planning Mistake Most People Make

One of the biggest mistakes professionals make is:

“I’ll start serious retirement planning later.”

But retirement wealth creation depends heavily on:

Time + Compounding

A person who starts investing early through disciplined SIPs often gains a massive long-term advantage.

Because:

Compounding works best over long periods.

Even moderate monthly SIP investing,

when continued consistently for decades,

can potentially create substantial long-term wealth.

This is exactly why disciplined investing behavior matters far more than short-term market excitement.

SIP Discipline Matters More Than Ever

For many salaried professionals,

SIPs remain one of the most practical approaches for retirement wealth creation.

Why?

Because SIPs help:

- create discipline,

- encourage consistency,

- reduce emotional investing,

- and support long-term compounding.

More importantly:

they create financial habits.

And wealth creation usually comes from:

behavioral discipline — not shortcuts.

This is also why Bangalore Inflation vs SIP Returns: Are You Actually Growing Wealth in 2026? became such an important topic for investors.

Because many professionals think they are “saving money”

while inflation quietly reduces real wealth creation.

The Real Estate Retirement Illusion

Many Bangalore professionals also assume:

“My apartment itself is my retirement plan.”

But relying ONLY on real estate can become risky.

Because:

- property is relatively illiquid,

- maintenance costs continue increasing,

- and real estate does not always create stable retirement cash flow.

This is exactly why Should Bangalore Techies Buy a Flat or Continue Renting in 2026? became such an important financial discussion.

Because retirement planning requires:

liquidity, flexibility, and diversified wealth creation.

Not just property ownership.

Social Media Has Created Unrealistic Retirement Expectations

Social media has made retirement planning even more confusing.

Today people constantly see:

- “Retire by 40” content,

- luxury lifestyle creators,

- exaggerated wealth stories,

- and unrealistic financial expectations.

This creates dangerous comparisons.

But the truth is:

There is NO universal retirement number.

Retirement planning depends on:

- lifestyle,

- family responsibilities,

- health,

- inflation,

- financial discipline,

- and long-term goals.

Blindly believing:

“₹2 crore is enough.”

Without proper planning, it can create serious retirement risks later.

So What Should Bangalore Professionals Actually Focus On?

Instead of obsessing over one fixed retirement number,

professionals should focus on building:

Long-Term Financial Systems

This includes:

- disciplined SIP investing,

- emergency funds,

- healthcare protection,

- proper insurance,

- controlled lifestyle inflation,

- and long-term investing consistency.

Because retirement security is usually built slowly through:

discipline and consistency.

Not shortcuts.

This is also why High Income Does NOT Automatically Create Financial Freedom became such an important financial realization for many salaried professionals.

Because:

wealth creation is behavioral — not emotional.

Final Thoughts

The ₹2 crore retirement dream once sounded enormous.

But Bangalore’s financial reality in 2026 is changing rapidly.

Due to:

- inflation,

- rising healthcare costs,

- lifestyle inflation,

- and longer life expectancy,

₹2 crore alone may no longer guarantee comfortable retirement security for many professionals.

This does NOT mean retirement is impossible.

It simply means:

retirement planning must become more realistic, disciplined, and long-term focused.

Ultimately:

Financial freedom is NOT created by chasing one random retirement number.

It is created through:

- disciplined investing,

- intelligent planning,

- controlled lifestyle inflation,

- and consistent long-term financial behavior.

At Niyyam, we strongly believe:

Wealth creation is not about speed. It is about discipline, patience, and consistency.

Frequently Asked Questions (FAQs)

1. Is ₹2 crore enough for retirement in Bangalore?

For many urban middle-class families,

₹2 crore alone may NOT provide comfortable retirement security for 25–35 years, especially after considering inflation and healthcare costs.

2. Why is retirement becoming more expensive?

Because:

- inflation is rising,

- healthcare costs are increasing rapidly,

- people are living longer,

- and urban lifestyles are becoming more expensive.

3. Why do high-income professionals still feel financially insecure?

Because:

- high EMIs,

- lifestyle inflation,

- weak savings discipline,

- and poor long-term planning

often reduce actual wealth creation.

4. Why are SIPs important for retirement planning?

SIPs help:

- build investing discipline,

- encourage consistency,

- support compounding,

- and create long-term wealth gradually.

5. Should retirement planning start early?

Absolutely YES.

The earlier someone starts investing,

the greater the long-term benefit of compounding.

Time is one of the most powerful retirement wealth creation tools.

Disclaimer

This article is intended purely for educational and informational purposes and should not be considered financial, investment, legal, or real estate advice.

Property investments and mutual fund investments involve risks and should be evaluated based on individual financial goals, affordability, liquidity needs, and risk appetite. Investors should conduct independent research and consult qualified financial advisors before making investment decisions.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply