By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

SIP vs SWP vs STP is one of the most important concepts in mutual fund investing, yet many investors do not fully understand how these strategies work together.

Mutual fund investing is not just about selecting the right fund.

It is equally important to understand:

- How to invest

- When to invest

- How to withdraw

This is where SIP, SWP, and STP play a critical role.

Many investors know these terms but struggle with:

- What each strategy actually does

- When to use each one

- How they fit into a complete financial plan

The truth is simple:

SIP builds wealth, STP optimizes investment timing, and SWP converts wealth into income.

If used correctly, these three strategies can help you create, manage, and utilize wealth efficiently.

💡 Key Takeaways

- SIP is ideal for long-term wealth creation

- STP helps manage lump sum investments efficiently

- SWP converts investments into a steady income

- Each strategy serves a different purpose

- Using all three creates a complete investment lifecycle

Direct Answer

SIP is used for regular investing and wealth creation, STP is used for gradually investing lump sum amounts to reduce timing risk, and SWP is used to generate regular income from accumulated investments.

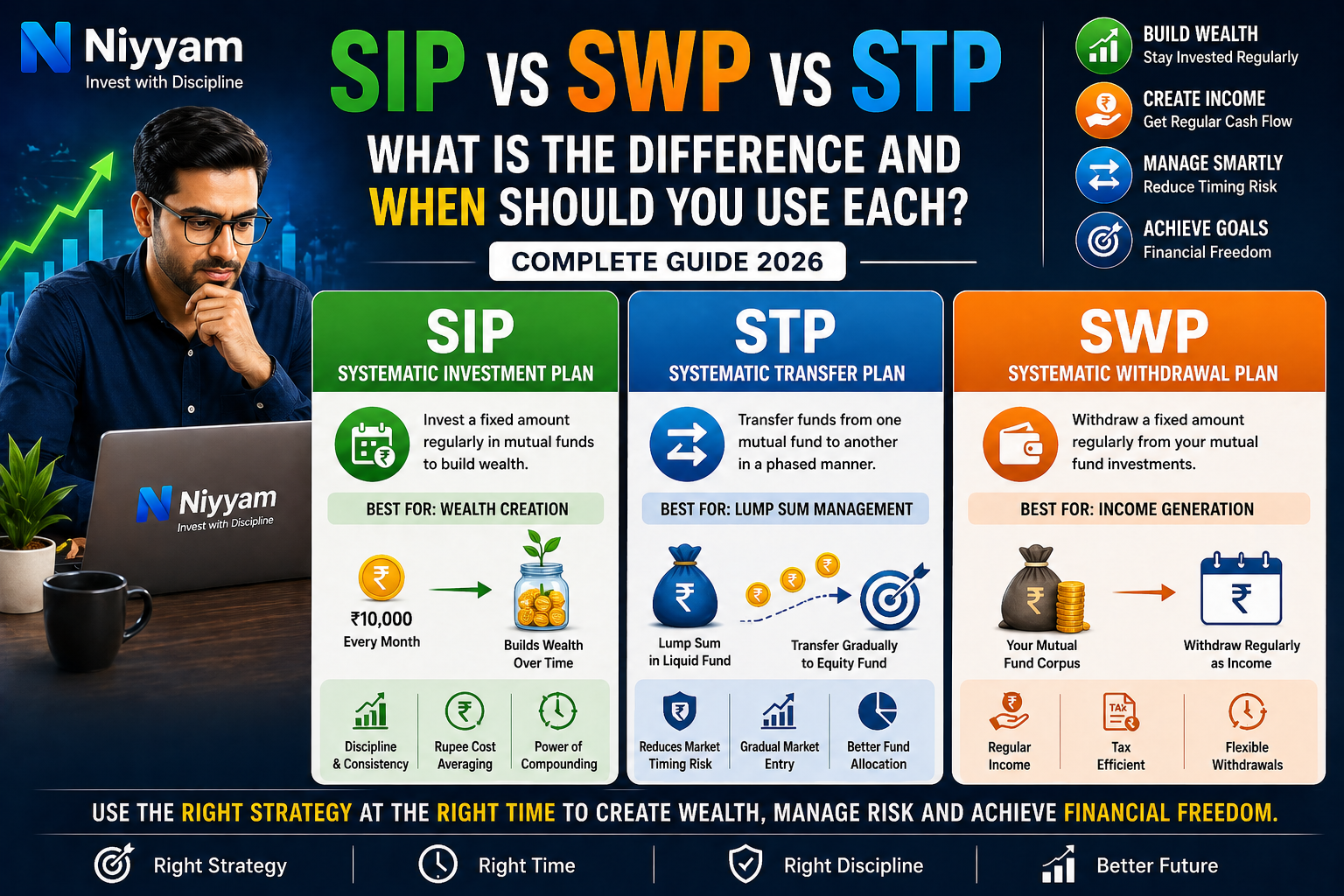

What is SIP (Systematic Investment Plan)?

SIP allows you to invest a fixed amount at regular intervals into a mutual fund.

Example

- ₹5,000 invested every month

- Units purchased consistently

Key Benefits

- Builds financial discipline

- Reduces market timing risk

- Enables rupee cost averaging

Important Insight

SIP is the most effective method for long-term wealth creation.

To understand SIP in detail, refer to

What is SIP in Mutual Funds? A Complete Beginner’s Guide (2026)

What is SWP (Systematic Withdrawal Plan)?

SWP allows you to withdraw a fixed amount from your mutual fund at regular intervals.

Example

- Investment: ₹20 lakh

- Monthly withdrawal: ₹20,000

Key Benefits

- Provides regular income

- Flexible withdrawals

- Better tax efficiency compared to traditional options

Important Insight

SWP helps convert accumulated wealth into a steady income stream.

To understand this better, refer to

SWP in Mutual Funds Explained: How to Create Monthly Income (2026 Guide)

What is STP (Systematic Transfer Plan)?

STP allows you to transfer funds from one mutual fund to another in a phased manner.

Example

- ₹5 lakh invested in a liquid fund

- ₹50,000 transferred monthly into an equity fund

Key Benefits

- Reduces timing risk

- Enables gradual market entry

- Helps manage lump sum investments efficiently

Important Insight

STP is the safest way to deploy large amounts into the market.

To understand lump sum investing, refer to

Lump Sum Investment Strategy in Mutual Funds: When and How to Invest (2026 Guide)

SIP vs SWP vs STP: Key Differences

| Feature | SIP | SWP | STP |

|---|---|---|---|

| Purpose | Investment | Withdrawal | Transfer |

| Money Flow | Bank → Fund | Fund → Bank | Fund → Fund |

| Ideal For | Wealth creation | Income generation | Lump sum deployment |

| Risk Impact | Reduces timing risk | Depends on withdrawal rate | Reduces entry risk |

Key Insight

These strategies are designed for different stages of your financial journey.

When Should You Use SIP?

Use SIP If:

- You have a regular income

- You are investing for long-term goals

- You want disciplined investing

Ideal For:

- Salaried individuals

- Beginners

- Long-term investors

Important Insight

SIP works best when combined with time and consistency.

To understand how SIP creates wealth, refer to

How SIP Builds Wealth Through Compounding (With Simple Examples)

When Should You Use STP?

Use STP If:

- You have a lump sum amount

- You want to avoid market timing

- You prefer gradual entry

Ideal For:

- Bonuses

- Inheritance

- Market uncertainty

Key Insight

STP protects you from investing all your money at the wrong time.

When Should You Use SWP?

Use SWP If:

- You need regular income

- You are retired or nearing retirement

- You want passive cash flow

Ideal For:

- Retirees

- Income-focused investors

Important Insight

SWP allows you to use your investments without immediately exhausting your capital.

How SIP, STP, and SWP Work Together

These strategies are not alternatives.

They complement each other.

Investment Lifecycle

Phase 1: Wealth Creation

Use SIP

Phase 2: Lump Sum Deployment

Use STP

Phase 3: Income Generation

Use SWP

Key Insight

A complete financial plan uses all three strategies at different stages.

Practical Example

Scenario

An investor follows a structured plan:

Step 1:

Invests ₹10,000/month via SIP

Step 2:

Receives ₹5 lakh bonus

Uses STP for gradual investment

Step 3:

Builds corpus over 15 years

Uses SWP for income

Outcome

- Wealth created

- Risk managed

- Income generated

Key Insight

The right strategy at the right time leads to optimal outcomes.

How to Choose Based on Life Stage

Early Career (20s–30s)

- Focus: Wealth creation

- Strategy: SIP

Mid Career (30s–40s)

- Focus: Growth + expansion

- Strategy: SIP + STP

Pre-Retirement (40s–50s)

- Focus: Capital protection

- Strategy: Balanced approach + STP

Retirement (50+)

- Focus: Income generation

- Strategy: SWP

Key Insight

Strategy selection depends more on your life stage than market conditions.

Common Mistakes to Avoid

- Using SWP too early

- Investing a lump sum without STP

- Stopping SIP during market downturns

- Confusing the purpose of strategies

Important Insight

Clarity of purpose leads to better investment decisions.

To avoid mistakes, refer to

How Not to Choose a Mutual Fund: 7 Critical Mistakes Investors Must Avoid (2026 Guide)

Quick Rule of Thumb

- Want to invest regularly → SIP

- Have lump sum → STP

- Need income → SWP

Golden Rule

Use the right strategy for the right purpose.

Frequently Asked Questions (FAQs)

Which is better — SIP, SWP, or STP?

All are useful for different purposes.

Can I use SIP and STP together?

Yes, they complement each other.

Is SWP safe?

Depends on withdrawal rate and fund selection.

What is best for beginners?

SIP is the best starting point.

Can I stop these anytime?

Yes, all are flexible.

Which strategy builds wealth fastest?

SIP with long-term discipline.

Conclusion

SIP, STP, and SWP are not alternatives.

They are three powerful tools designed for different stages of your financial journey.

Final Thought

Most investors struggle not because they lack knowledge,

but because they use the wrong strategy at the wrong time.

If you understand when and how to use SIP, STP, and SWP:

- You can build wealth efficiently

- Manage risk effectively

- Generate income when needed

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply