By Ashok Prasad, Founder, Niyyam

Published: March 2026

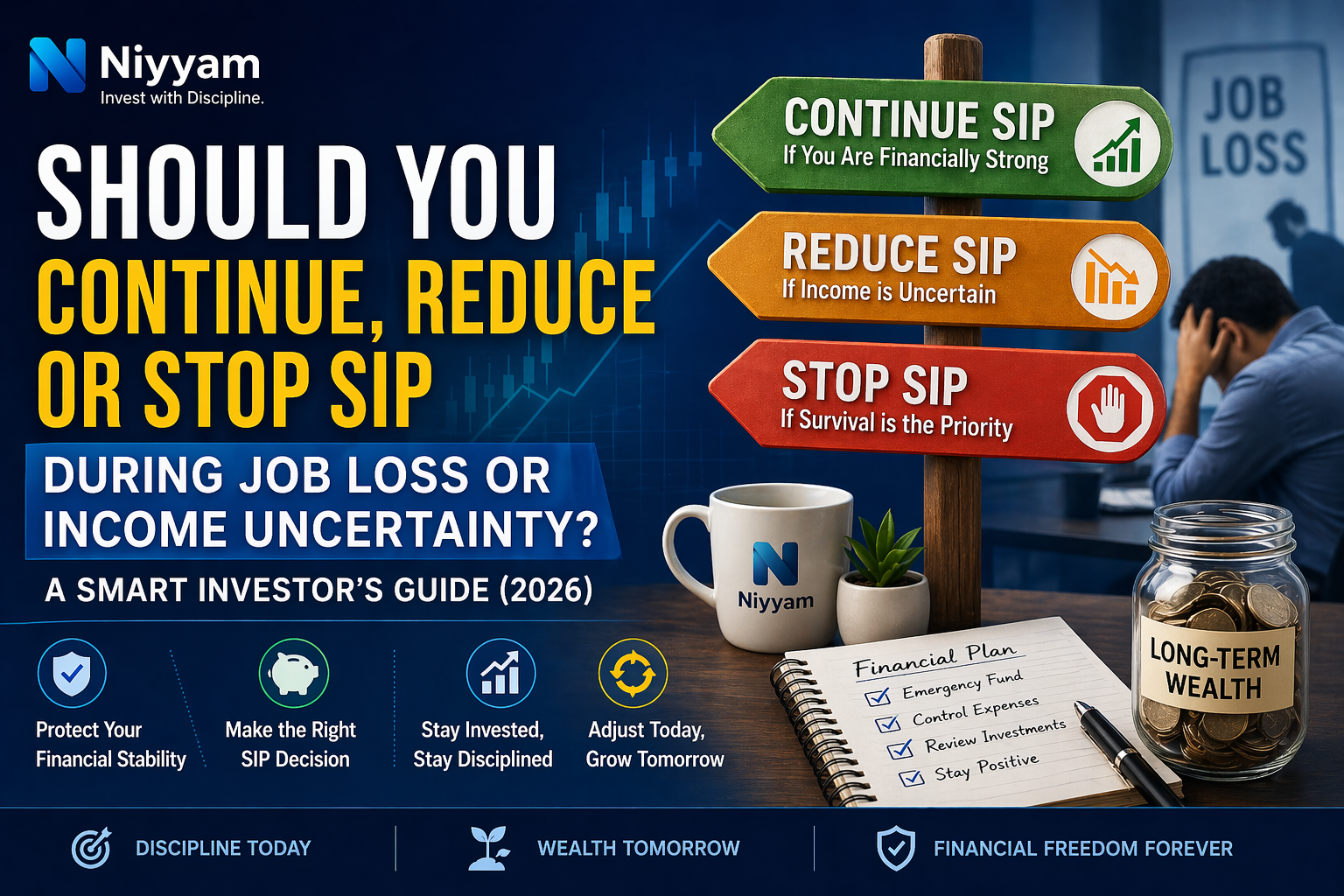

Introduction: Should You Continue SIP During Job Loss?

Should you continue SIP during job loss is one of the most important financial decisions an investor will face.

When income becomes uncertain, your financial priorities change completely. Instead of focusing only on wealth creation, your primary goal shifts to survival, stability, and cash flow management.

Many investors panic during such phases and take extreme actions like stopping SIPs completely or redeeming investments. On the other hand, some continue SIPs blindly without assessing their financial situation, which can also create stress.

The correct approach lies in balance.

You need to decide whether to continue SIP during job loss, reduce it, or pause it based on your financial strength—not emotions.

A structured decision can:

- Protect your financial stability

- Preserve your long-term investments

- Maintain discipline without stress

A wrong decision can:

- Break your investment journey

- Create unnecessary losses

- Increase financial pressure

💡 Key Takeaways

- Do not stop SIP blindly during a job loss

- Your emergency fund determines your decision

- Continue SIP if you have a strong financial backup

- Reduce SIP if income is uncertain but manageable

- Pause SIP only when survival is at risk

- Avoid redeeming investments unnecessarily

- SIP flexibility allows easy restart anytime

Direct Answer

Should you continue SIP during job loss depends entirely on your financial situation. You should continue, reduce, or pause SIP based on your emergency fund, expenses, and income visibility. The goal is to balance survival and long-term investing.

Step 1: Assess Your Financial Situation Clearly

Before making any decision, you must evaluate your current financial condition in detail.

Key Questions to Ask

- How many months can you survive without income

- Do you have an emergency fund

- What are your fixed monthly expenses

- Do you have any alternate income source

- Do you have dependents relying on you

Emergency Fund-Based Decision Framework

- 6–12 months expenses → Continue SIP

- 3–6 months expenses → Reduce SIP

- Less than 3 months → Pause SIP

Your decision about whether to continue SIP during job loss should always be based on financial strength—not market conditions.

Understanding SIP in the Bigger Picture

SIP is designed for long-term investing and works across market cycles.

Temporary interruptions do not destroy wealth. What matters is consistency over time.

To understand this deeply, you can explore

How SIP Builds Wealth Through Compounding (With Simple Examples)

Option 1: Continue SIP When Financially Strong

If your financial condition is stable, continuing SIP is the best decision.

When Should You Continue SIP

- You have 6–12 months of emergency funds

- Your expenses are under control

- You have alternative or expected income

- Your investment horizon is long-term

Benefits of Continuing SIP

- Lower average cost during market downturns

- Compounding continues uninterrupted

- Discipline remains intact

- Avoid emotional decision-making

- Better long-term returns

Investors who continue SIP during uncertain times often benefit the most in the long run.

Option 2: Reduce SIP When Income Is Uncertain

Reducing SIP is the most practical approach for many investors.

When Should You Reduce SIP

- Emergency fund is between 3–6 months

- Income is partially affected

- Expenses are manageable but tight

Example

- Original SIP: ₹10,000

- Reduced SIP: ₹4,000 to ₹6,000

Why This Strategy Works

- Maintains market participation

- Preserves liquidity

- Reduces financial stress

- Keeps your investment habit intact

To scale your SIP later, you can refer to

How to Increase SIP Amount Over Time (Step-Up SIP Strategy for 2026 Investors)

Option 3: Pause SIP When Survival Is Priority

If your financial situation is weak, pausing SIP is the right decision.

When Should You Pause SIP

- No income source

- Emergency fund less than 3 months

- High financial pressure

- Existing liabilities like EMIs

Important Insight

Pausing SIP is not a failure—it is a financially responsible decision.

What You Must Avoid

- Panic selling investments

- Redeeming funds unnecessarily

- Stopping SIP without evaluation

To understand the long-term impact, you can also read

What Happens When You Stop SIP? Complete Impact Explained (2026 Investor Guide)

Quick Rule of Thumb

- Strong finances → Continue SIP

- Moderate uncertainty → Reduce SIP

- Severe stress → Pause SIP

Always take decisions based on logic, not fear.

Step 2: Prioritize Financial Survival

When income is uncertain, your priorities must shift.

Priority Order

- Essential expenses

- Emergency fund

- Insurance

- Investments

Your SIP should never compromise your financial survival.

Step 3: Optimize Expenses Before Stopping SIP

Before stopping SIP, try reducing your expenses.

Expense Optimization Strategy

- Cancel unnecessary subscriptions

- Reduce lifestyle expenses

- Negotiate fixed costs

- Restructure EMIs if required

This approach may help you continue SIP even in difficult situations.

Step 4: Avoid Emotional Decisions

Most financial mistakes happen due to emotions.

Common Emotional Triggers

- Fear leads to unnecessary SIP stoppage

- Panic leads to selling investments

- Stress leads to poor financial decisions

To understand this better, you can also explore

Why Most SIP Investors Fail to Build Wealth (And How to Avoid It in 2026)

Real-Life Scenario Analysis

Scenario 1: Strong Financial Position

- Emergency fund: 10 months

- Income: Temporary disruption

- Expenses: Controlled

Action: Continue SIP

Scenario 2: Moderate Situation

- Emergency fund: 4 months

- Income: Reduced

- Expenses: Stable

Action: Reduce SIP

Scenario 3: High Risk

- Emergency fund: 1–2 months

- Income: No income

- Expenses: High

Action: Pause SIP

Advanced Insight: Flexible SIP Strategy

SIP is not rigid—it can be adjusted based on your situation.

Flexible Options

- Reduce SIP temporarily

- Pause and restart later

- Avoid withdrawing investments

Flexibility helps protect both liquidity and long-term compounding.

To understand investing during tough conditions, refer to

How to Invest During Market Crash in Mutual Funds (Smart Strategy for 2026 Investors)

What Happens If You Make the Wrong Decision

Making the wrong SIP decision during job loss can:

- Break long-term compounding

- Cause unnecessary losses

- Increase financial stress

Balance is the key.

How to Restart SIP After Recovery

Once your income stabilizes, restarting SIP should be done properly.

Restart Plan

- Restart SIP immediately

- Start with a smaller amount

- Increase gradually

- Use step-up SIP

You can also refer to

How to Restart SIP After Stopping (2026 Guide)

Common Mistakes to Avoid

- Stopping SIP without analysis

- Redeeming investments unnecessarily

- Ignoring the importance of an emergency fund

- Trying to time the market

- Overreacting to temporary situations

Conclusion: Take a Balanced Decision

There is no one-size-fits-all answer.

The right decision depends entirely on your financial condition.

- Protect your survival first

- Stay flexible

- Maintain discipline

- Think long-term

Final Verdict

Should you continue SIP during job loss depends on your financial strength.

- Continue SIP if stable

- Reduce SIP if uncertain

- Pause SIP if under stress

You do not need to stop investing—you need to adjust intelligently.

Final Thought

Wealth creation is not about rigid investing rules.

It is about adapting your strategy based on life situations.

Stay calm, think logically, and make decisions that support both your present and your future.

Frequently Asked Questions

1. Should I continue SIP during job loss

Yes, if you have a strong emergency fund.

2. Is it okay to pause SIP

Yes, if your financial stability is at risk.

3. Should I redeem mutual funds during job loss

Only if absolutely necessary.

4. Can I restart SIP after stopping

Yes, SIP can be restarted anytime.

5. How much emergency fund is needed

Ideally 6–12 months of expenses.

6. Is reducing SIP better than stopping

Yes, in most cases.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply