By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

If you are wondering how to build 10 lakh mutual fund portfolio effectively, you are not alone. Building a ₹10 lakh portfolio may sound like a big milestone.

But in reality, it is one of the most achievable financial goals for Indian investors today.

The real challenge is not reaching ₹10 lakh.

The real challenge is building it the right way.

Most investors struggle not because they lack money, but because they lack structure.

They tend to:

- Invest randomly without a clear plan

- Choose funds based on tips or recent performance

- Ignore asset allocation

- Panic during market corrections

Because of these mistakes, even after investing lakhs, they fail to create meaningful long-term wealth.

If you want your ₹10 lakh portfolio to grow into ₹25–40 lakh over time, you need a clear, disciplined, and structured approach.

Before building your portfolio, it is important to understand

Which Mutual Funds Should You Avoid in 2026? (Red Flags Every Investor Must Know)

because avoiding poor-quality funds is the first step toward building a strong portfolio.

💡 Key Takeaways

- Asset allocation is more important than fund selection

- Diversification across market caps is essential

- Debt funds provide stability and reduce risk

- SIP and lump sum combination works best

- Avoid over-diversification

- Portfolio review is critical

- Consistency matters more than timing

Direct Answer

To build a ₹10 lakh mutual fund portfolio, allocate 60–70% to equity, 20–30% to debt, and around 10% to hybrid funds. Diversify across large, mid, and small caps, invest using a mix of SIP and lump sum, and review your portfolio annually for long-term wealth creation.

Step 1: Define Your Goal and Time Horizon

Before investing even ₹1, you must clearly define:

- Why are you investing?

- When will you need this money?

Goal-Based Planning

- Short-term (1–3 years): Debt-focused

- Medium-term (3–5 years): Hybrid allocation

- Long-term (5+ years): Equity-focused

If your goal is long-term wealth creation, equity mutual funds should form the core of your portfolio.

Time horizon directly impacts your ability to take risk.

The longer you stay invested, the better your chances of handling volatility and earning higher returns.

Step 2: Decide Asset Allocation

Asset allocation is the foundation of your portfolio.

It determines:

- Your risk level

- Your return potential

- Your stability during market fluctuations

Ideal ₹10 Lakh Allocation

- Equity Funds: ₹6,50,000 (65%)

- Debt Funds: ₹2,50,000 (25%)

- Hybrid Funds: ₹1,00,000 (10%)

Why This Allocation Works

- Equity drives long-term growth

- Debt reduces volatility

- Hybrid adds balance

To understand fund categories better, refer to

Large Cap vs Mid Cap vs Small Cap Funds: Where Should You Invest?

Asset allocation alone can decide the success or failure of your portfolio.

Step 3: Break Down Equity Allocation

Avoid putting all your equity investment into one category.

Equity Distribution

- Large Cap: 40%

- Mid Cap: 35%

- Small Cap: 25%

Why This Matters

Large-cap funds provide stability during market downturns.

Mid-cap funds offer higher growth potential.

Small-cap funds provide high return opportunities but come with higher risk.

A balanced mix ensures that your portfolio performs well across different market cycles.

Step 4: Keep Your Portfolio Simple

Many investors believe that more funds mean better diversification.

This is incorrect.

Ideal Portfolio Structure

- 1 Large Cap Fund

- 1 Flexi or Mid Cap Fund

- 1 Small Cap Fund

- 1 Debt Fund

- 1 Hybrid Fund

If you are unsure how to evaluate funds, refer to

How to Choose the Right Mutual Fund in India (A Beginner’s Practical Guide)

A simple portfolio is easier to track, manage, and maintain.

Step 5: SIP vs Lump Sum Strategy

How you invest matters as much as where you invest.

Investment Approach

- Monthly income: SIP

- Bonus or surplus: Lump sum

- Market uncertainty: Prefer SIP

Ideal Strategy

- 60–70% via SIP

- 30–40% via lump sum

To understand this better, read

SIP vs Lump Sum: Which Investment Strategy Is Better for Beginners?

This combination helps reduce risk while taking advantage of market opportunities.

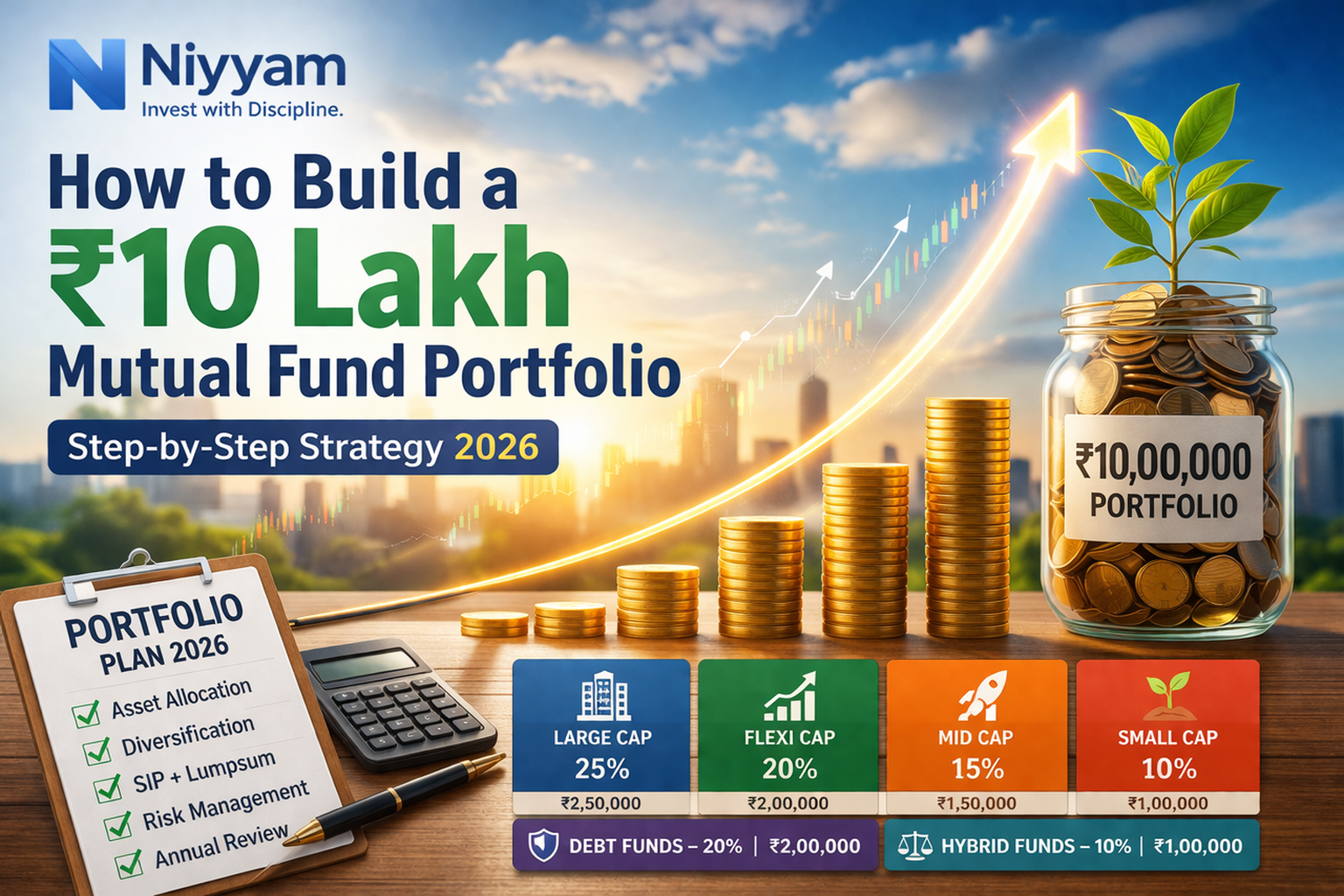

Step 6: Example ₹10 Lakh Portfolio

Here is a practical example:

- Large Cap Fund: ₹2,50,000

- Flexi Cap Fund: ₹2,00,000

- Mid Cap Fund: ₹1,50,000

- Small Cap Fund: ₹1,00,000

- Debt Fund: ₹2,00,000

- Hybrid Fund: ₹1,00,000

This structure balances growth, risk, and stability effectively.

Step 7: Rebalancing Strategy

Over time, your portfolio allocation will change due to market movements.

Example

- Equity increases from 65% to 75%

- Debt reduces significantly

What You Should Do

- Rebalance once a year

- Restore original allocation

Rebalancing ensures that your portfolio does not become overly risky.

Step 8: Risk Management

Every portfolio must manage risk.

Common Risks

- Market volatility

- Overexposure to small caps

- Lack of diversification

How to Manage Risk

- Maintain proper debt allocation

- Avoid too many funds

- Review regularly

Managing downside risk is more important than chasing high returns.

Common Mistakes to Avoid

- Investing without allocation

- Choosing too many funds

- Ignoring debt allocation

- Chasing past returns

- Stopping investments during market corrections

To avoid these, read

7 Common SIP Mistakes New Investors Make (And How to Avoid Them)

Advanced Insight

Most investors focus on:

“Which fund should I pick?”

Smart investors focus on:

“How should my portfolio be structured?”

Reality

- Random investing leads to average results

- Structured investing leads to strong compounding

Power of Compounding

If ₹10 lakh grows at:

- 10% → ₹25.9 lakh

- 12% → ₹31 lakh

- 15% → ₹40.5 lakh

Even small improvements in returns can significantly impact long-term wealth.

Conclusion

Building a ₹10 lakh portfolio is not difficult.

But building it correctly makes all the difference.

If you:

- Allocate properly

- Diversify wisely

- Stay consistent

Your ₹10 lakh can become a powerful wealth-building engine.

Final Verdict

- Start with proper allocation

- Keep your portfolio simple

- Combine SIP and lump sum

- Review annually

A disciplined portfolio always performs better than a random one.

Final Thought

Wealth is not created by investing more.

It is created by investing wisely and consistently.

Frequently Asked Questions (FAQs)

1. How many mutual funds should I hold?

Ideally, 4–6 funds.

2. Is ₹10 lakh enough to start investing?

Yes, it is a strong starting point.

3. Should I invest all at once?

No, combine SIP and lump sum.

4. How often should I rebalance?

Once a year is sufficient.

5. Can SIP alone build this portfolio?

Yes, but it will take time.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply