By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

If you are a business owner or freelancer, your financial life is very different from a salaried individual.

Your income is:

- Irregular

- Unpredictable

- Sometimes very high, sometimes very low

And because of this, your investment strategy cannot be the same as that of salaried investors.

Yet, many freelancers and business owners:

- Invest randomly when they earn more

- Stop investing when income drops

- Ignore asset allocation

- Take excessive risk during good times

This leads to:

- Inconsistent wealth creation

- Poor financial stability

- High stress during downturns

If you want to build long-term wealth, you need a flexible but disciplined mutual fund strategy.

Before building your strategy, it’s helpful to understand

Best Mutual Fund Strategy for Salaried Individuals in India (2026 Complete Guide) — so you can clearly see how your approach should differ.

💡 Key Takeaways

- Income irregularity requires flexible investment planning

- An emergency fund is more critical for salaried individuals

- A combination of SIP + opportunistic lump sum works best

- Asset allocation must be dynamic, not fixed

- Avoid overexposure to high-risk funds

- Maintain liquidity to handle business cycles

- Discipline during high-income phases is crucial

- Wealth is built by consistency, not income spikes

Direct Answer

The best mutual fund strategy for business owners and freelancers in 2026 is to maintain a strong emergency fund, invest through a mix of flexible SIP and lump sum, diversify across equity and debt, and adjust asset allocation based on income stability while maintaining long-term discipline.

Why Business Owners Need a Different Strategy

Your income pattern defines your strategy.

Income Comparison

| Factor | Salaried | Business Owner |

|---|---|---|

| Income stability | High | Low |

| Predictability | Fixed | Variable |

| Investment style | SIP | Flexible |

Reality of Freelancers

- Income can fluctuate monthly

- Cash flow management becomes critical

- Risk tolerance changes frequently

If you blindly follow aggressive strategies, you may fall into the mistakes explained in

Which Mutual Funds Should You Avoid in 2026? (Red Flags Every Investor Must Know).

{kind=link}

Key Point:

Your strategy must adapt to your income volatility.

Step 1: Build a Larger Emergency Fund

This is non-negotiable.

Recommended Emergency Fund

| Monthly Expense | Required Fund |

|---|---|

| ₹50,000 | ₹6 – ₹9 lakh |

| ₹1,00,000 | ₹12 – ₹18 lakh |

| ₹2,00,000 | ₹24 – ₹36 lakh |

Why More is Needed

- No guaranteed income

- Business downturn risk

- Client payment delays

Where to Keep It

- Liquid funds

- Ultra short-term debt funds

- Savings account

Key Point:

An emergency fund is your financial survival tool.

Step 2: Flexible Investment Strategy (Very Important)

Unlike salaried individuals, you cannot rely only on SIP.

Best Investment Approach

| Low-income phase | Strategy |

|---|---|

| Stable income phase | SIP |

| High income phase | Lumpsum |

| Low income phase | Pause SIP |

Example

| Month | Income | Action |

|---|---|---|

| Jan | High | Lumpsum invest |

| Feb | Medium | SIP |

| Mar | Low | Skip/Reduce |

Key Point:

Flexibility is your biggest advantage — use it wisely.

Step 3: Asset Allocation Strategy

Your allocation should be slightly conservative.

Ideal Allocation

| Risk Profile | Equity | Debt | Hybrid |

|---|---|---|---|

| Moderate | 60% | 30% | 10% |

| Aggressive | 70% | 20% | 10% |

Why This Works

- Equity → Growth

- Debt → Stability during low income

- Hybrid → Balance

To understand fund categories better, refer to

Large Cap vs Mid Cap vs Small Cap Funds Explained (2026 Guide).

{kind=link}

Key Point:

Debt allocation is your safety cushion.

Step 4: Equity Allocation Breakdown

Avoid putting all money into high-risk funds.

Equity Mix

| Category | Allocation |

|---|---|

| Large Cap | 35–40% |

| Flexi Cap | 20–25% |

| Mid Cap | 15–20% |

| Small Cap | 10–15% |

Why Important

- Reduces volatility

- Ensures smoother returns

- Prevents panic during downturns

Step 5: Maintain Liquidity

Liquidity is critical for business owners.

Liquidity Allocation

| Type | Allocation |

|---|---|

| Emergency Fund | 6–12 months |

| Liquid Investments | 5–10% portfolio |

Why It Matters

- Covers unexpected expenses

- Avoids forced selling of investments

Key Point:

Liquidity prevents bad financial decisions.

Step 6: Limit Number of Funds

Keep your portfolio simple.

Ideal Fund Count

| Portfolio Size | Funds |

|---|---|

| Up to ₹10 lakh | 3–5 |

| ₹10L–₹50L | 4–6 |

Suggested Structure

- 2 Equity Funds

- 1 Mid/Small Cap Fund

- 1 Debt Fund

- 1 Hybrid Fund

If you’re unsure about selection, refer to

How to Choose the Best Mutual Fund in India (2026 Guide).

Key Point:

Simplicity improves decision-making.

Step 7: Opportunistic Investing (Your Advantage)

You have one big advantage:

You can invest more when income is high.

Strategy Table

| Market Condition | Action |

|---|---|

| Market crash | Invest lumpsum |

| Bull market | Continue SIP |

| High income | Increase allocation |

This strategy works well when combined with

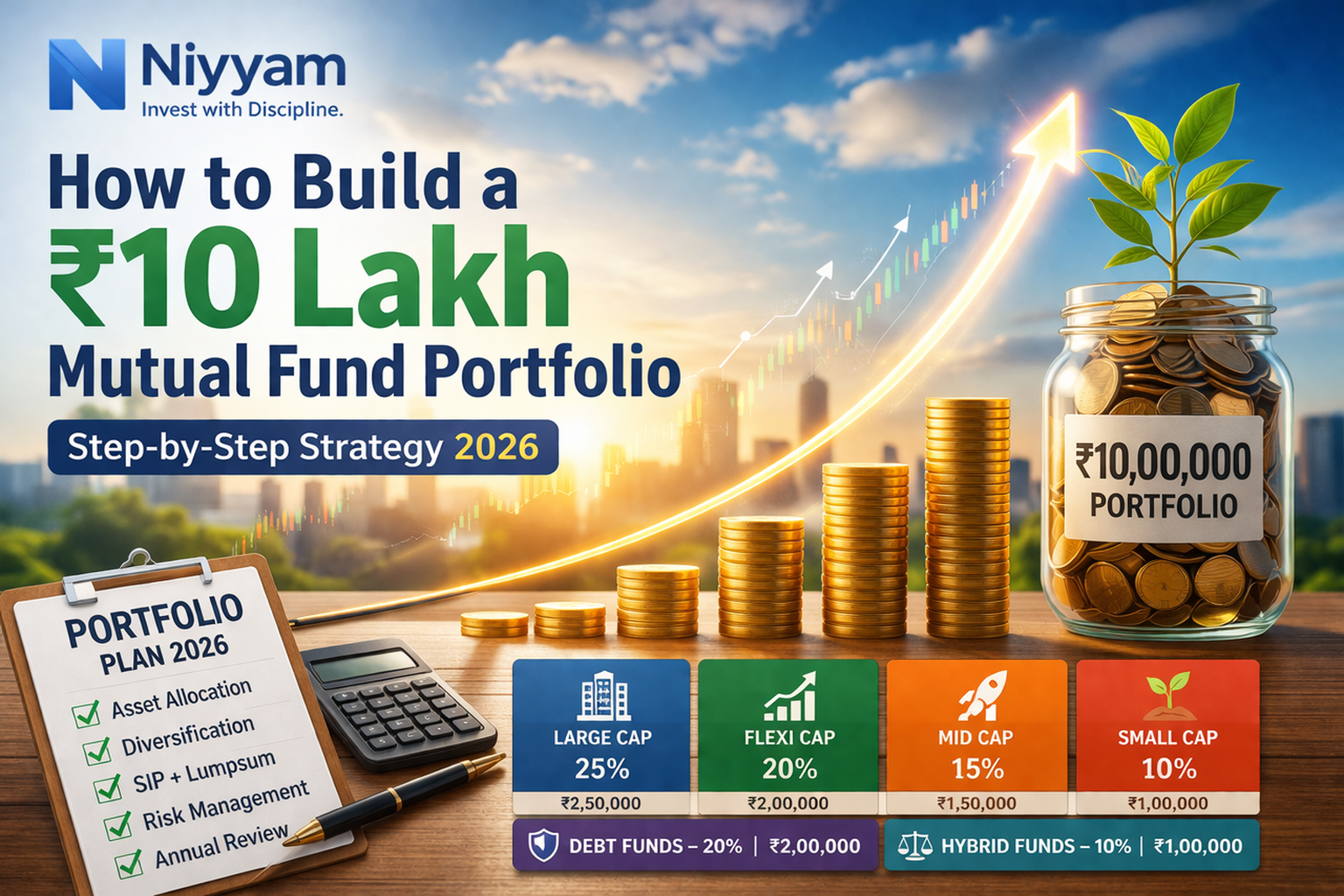

How to Build a ₹10 Lakh Mutual Fund Portfolio (Step-by-Step Strategy 2026).

{kind=link}

Key Point:

Use income spikes to accelerate wealth.

Step 8: Risk Management

Business owners face a higher risk.

Key Risks

- Income volatility

- Market fluctuations

- Business downturn

Risk Control Table

| Risk | Solution |

|---|---|

| Income drop | Emergency fund |

| Market fall | Continue investing |

| Overexposure | Rebalance |

Key Point:

Survival is more important than returns.

Quick Rule of Thumb

- Maintain a 6–12 months emergency fund

- Use SIP + lump sum combination

- Keep 20–30% in debt

- Avoid aggressive investing during unstable income

- Stay consistent during good phases

Common Mistakes Business Owners Make

- Investing only during high-income months

- Ignoring the emergency fund

- Over-investing in small caps

- Not maintaining liquidity

- Taking excessive risk

Impact Table

| Mistake | Result |

|---|---|

| No liquidity | Forced withdrawals |

| Over-risk | High losses |

| No planning | Inconsistent wealth |

Advanced Insight (Very Important)

Business owners often believe:

“Higher income means higher wealth.”

This is not true.

Reality

| Factor | Impact |

|---|---|

| Income | Variable |

| Investment discipline | Critical |

| Wealth creation | Depends on consistency |

Example

| Investor Type | Outcome |

|---|---|

| High income, no discipline | Low wealth |

| Moderate income, disciplined | High wealth |

Key Point:

Consistency matters more than income spikes.

Conclusion

Business owners and freelancers have:

- Higher earning potential

- Higher risk

- Greater flexibility

If you combine flexibility with discipline, you can create extraordinary wealth.

Final Verdict

- Build strong emergency fund

- Use flexible investing approach

- Maintain balanced allocation

- Stay disciplined during high-income phases

A smart strategy turns irregular income into consistent wealth.

Final Thought

Your income may be unpredictable.

Your wealth creation should not be.

Frequently Asked Questions (FAQs)

1. Should freelancers invest through SIP?

Yes, but keep it flexible.

2. How much emergency fund is required?

At least 6–12 months of expenses.

3. Can I skip debt funds?

No, debt funds provide stability.

4. When should I invest lumpsum?

During high income or market dips.

5. Is small cap suitable for business owners?

Yes, but limited exposure only.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply