By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

ELSS mutual funds tax benefit is one of the most important aspects investors consider while planning tax-saving investments in India, especially under the old tax regime.

When it comes to saving tax, most investors look for simple and familiar options:

- Tax-saving fixed deposits

- Public Provident Fund (PPF)

- Insurance-linked plans

However, there is one option that not only helps in tax saving but also offers long-term wealth creation potential:

ELSS Mutual Funds (Equity Linked Savings Scheme)

But in 2026, there is a critical update:

ELSS tax benefits depend on the tax regime you choose.

If you misunderstand this, you may invest expecting tax savings that you may not receive.

In this guide, you will learn:

- What ELSS mutual funds are

- How tax benefits work in the old vs new regime

- Why ELSS is still relevant without tax benefits

- How to use ELSS for long-term wealth creation

💡 Key Takeaways

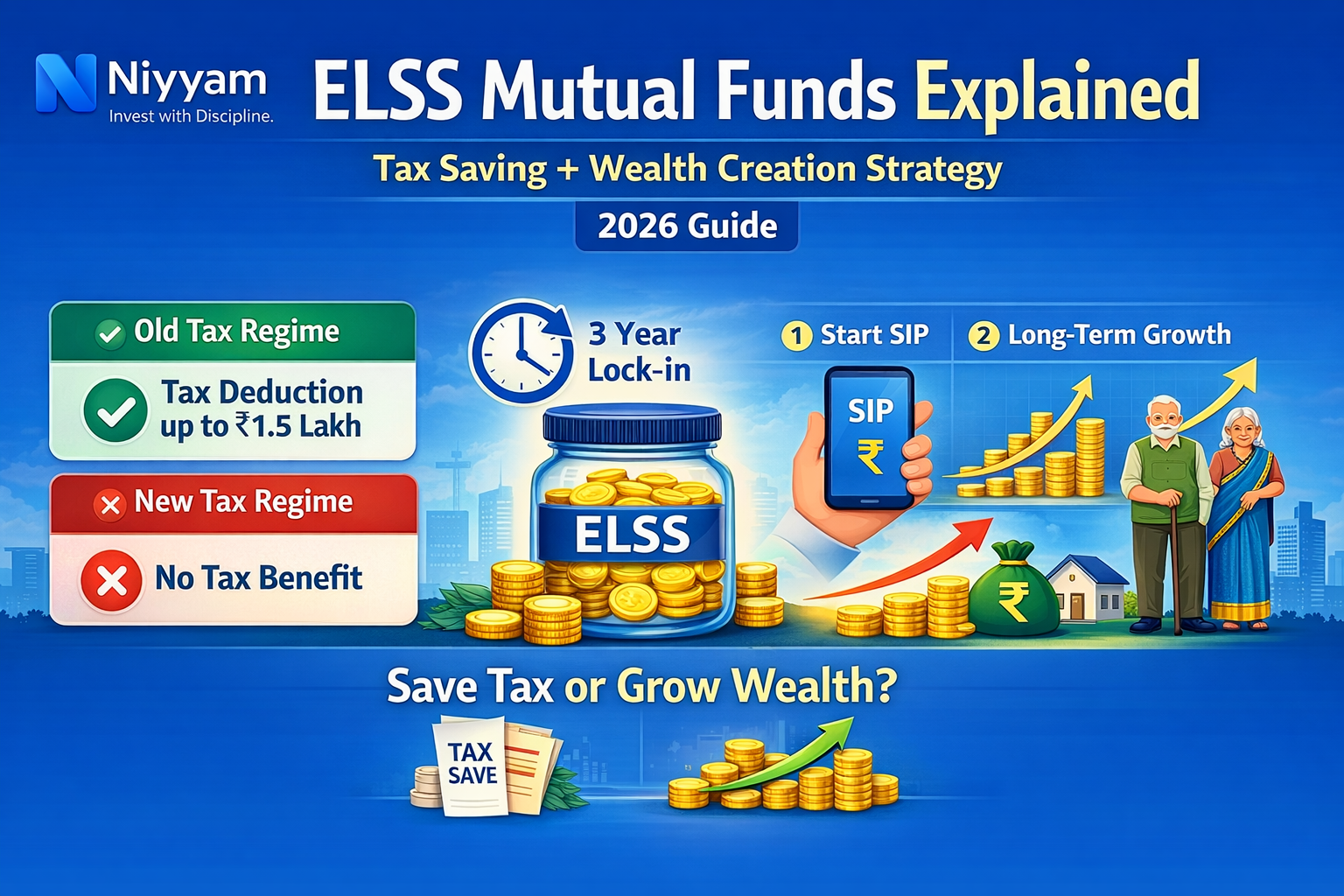

- ELSS offers tax deduction up to ₹1.5 lakh under Section 80C (old regime only)

- No tax benefit under the new tax regime

- 3-year lock-in is the shortest among tax-saving options

- Equity exposure provides higher return potential

- ELSS should be used for wealth creation, not just tax saving

Direct Answer

Does ELSS mutual funds provide tax benefits in 2026?

ELSS mutual funds provide tax benefits only under the old tax regime through Section 80C deductions up to ₹1.5 lakh. Under the new tax regime, ELSS does not offer any tax benefit and should be treated as a pure investment option.

What is an ELSS Mutual Fund?

ELSS (Equity Linked Savings Scheme) is a type of equity mutual fund that invests primarily in stocks.

Key Features

- Invests mainly in equities

- Mandatory lock-in period of 3 years

- Potential for higher long-term returns

Simple Understanding

ELSS is a mutual fund that combines:

- Tax saving (in old regime)

- Wealth creation (long-term)

ELSS Mutual Funds Tax Benefit (Updated for 2026)

This is the most important section every investor must understand.

Under the Old Tax Regime

- ELSS qualifies under Section 80C

- You can claim a deduction up to ₹1.5 lakh

- This reduces your taxable income

Example

- Income: ₹8 lakh

- ELSS investment: ₹1.5 lakh

Taxable income becomes ₹6.5 lakh

Under the New Tax Regime

- No Section 80C deductions allowed

- ELSS does not provide tax benefit

Key Insight

- Old regime: ELSS = tax saving + investment

- New regime: ELSS = only investment

Important Rule

Always decide your tax regime before investing in ELSS.

Lock-in Period: Why It Matters

ELSS comes with a mandatory 3-year lock-in.

What This Means

- You cannot withdraw before 3 years

- Each SIP installment has a separate lock-in

Why This is Beneficial

- Encourages long-term investing

- Prevents emotional decisions

- Supports compounding

Key Insight

ELSS has the shortest lock-in among all tax-saving instruments.

ELSS vs Other Tax Saving Options

ELSS vs PPF

- ELSS: Market-linked, higher return potential

- PPF: Fixed return, very low risk

ELSS vs Tax-Saving FD

- ELSS: Can beat inflation

- FD: Fixed returns, often lower after tax

ELSS vs Insurance Plans

- ELSS: Transparent and flexible

- Insurance: Complex and often lower returns

Key Insight

ELSS offers growth potential that traditional options may not provide.

Returns in ELSS Mutual Funds

Since ELSS invests in equities, returns are market-linked.

Expected Returns

- Long-term average: 10% to 14%

Important Understanding

- Returns are not guaranteed

- Short-term volatility is normal

- Long-term growth can be significant

Refer to How Mutual Funds Generate Returns for Investors (With Simple Examples).

ELSS as a Wealth Creation Tool

Even without tax benefits, ELSS remains a powerful investment.

Why

- Equity exposure

- Long-term compounding

- Built-in discipline due to lock-in

Example

- Investment: ₹1.5 lakh per year

- Duration: 15 years

- Return: 12%

Total investment: ₹22.5 lakh

Value: ₹50+ lakh

Key Insight

ELSS should not be used only for tax savings.

It should be used for long-term wealth creation.

How to Invest in ELSS

Lump Sum

- Invest once

- Suitable during market corrections

SIP (Recommended)

- Invest monthly

- Reduces timing risk

- Builds discipline

Best Strategy

Start SIP early instead of investing in March.

Refer to What is SIP in Mutual Funds? A Complete Beginner’s Guide (2026).

How to Choose the Right ELSS Fund

1. Long-Term Performance

Check 5 to 10-year returns

2. Consistency

Avoid unstable funds

3. Expense Ratio

Lower cost improves returns

4. Investment Strategy

Choose clear strategies

Refer to How to Compare Mutual Funds in India (5 Key Metrics Every Investor Must Check).

Where ELSS Fits in Your Portfolio

Suggested Allocation

- 50% to 70% equity funds

- 10% to 20% ELSS

- Remaining in debt

Key Insight

Do not over-allocate to ELSS.

Treat it as part of equity allocation.

Common Mistakes to Avoid

- Investing only for tax savings

- Waiting until March

- Exiting after lock-in

- Choosing too many ELSS funds

Important Insight

ELSS is not a short-term product.

ELSS Strategy for 2026 Investors

Step-by-Step Plan

- Decide your tax regime

- Start SIP early

- Invest consistently

- Hold beyond 3 years

- Combine with other funds

- Review periodically

Real-Life Scenario: ELSS with and without Tax Benefit

Investor A (Old Regime)

- Gets tax benefit

- Builds wealth

Investor B (New Regime)

- No tax benefit

- Still benefits from growth

Key Insight

ELSS remains valuable even without tax benefits.

Conclusion

The tax benefit of ELSS mutual funds depends on your tax regime.

- Old regime: tax saving + investment

- New regime: pure investment

ELSS is not just a tax-saving tool.

It is a long-term wealth creation instrument.

Final Thought

Do not invest in ELSS just to save tax.

Invest to build wealth.

Frequently Asked Questions (FAQs)

1. Does ELSS provide tax benefit in 2026?

Only under the old tax regime.

2. Is ELSS useful in the new regime?

Yes, for wealth creation.

3. What is the lock-in period?

3 years.

4. Is ELSS risky?

It carries market risk but offers long-term growth potential.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply