By Ashok Prasad, Founder, Niyyam

Published: March 2026

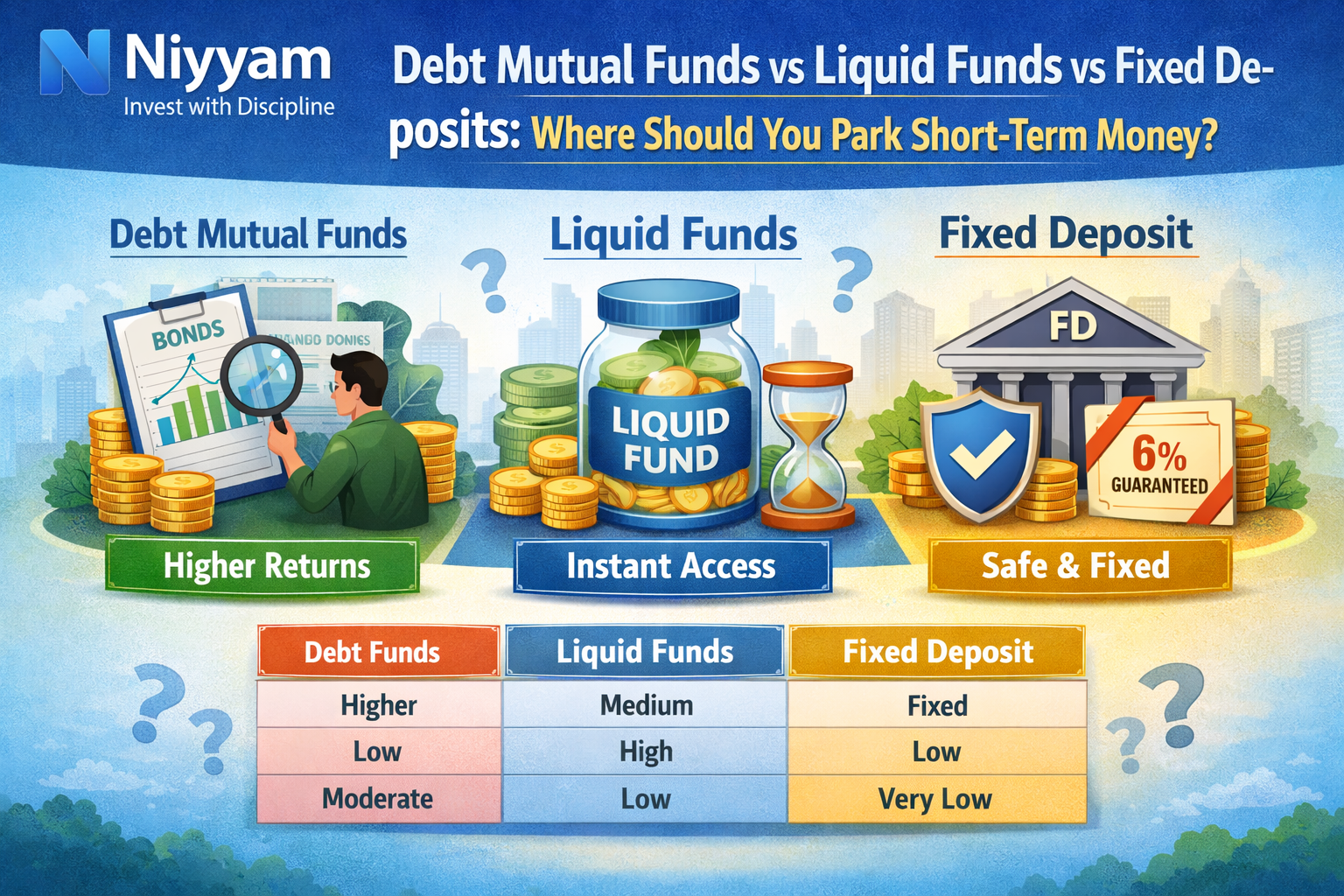

FD vs liquid fund vs debt fund — which one should you choose for short-term investing?

If you’re trying to park money safely for a few months or years, choosing the wrong option can cost you returns, liquidity, or even peace of mind.

When it comes to short-term money (typically 1–3 years), investors often face a common confusion:

- Should you choose fixed deposits for safety?

- Use liquid funds for flexibility?

- Or consider debt mutual funds for better returns?

This decision is critical because:

- You cannot afford high risk in short-term goals

- You still want better returns than a savings account

- You need liquidity and safety together

Choosing the wrong option can lead to:

- Capital loss

- Liquidity issues

- Missed opportunities

The correct approach is not choosing one blindly, but understanding where each option fits best.

💡 Key Takeaways

- Fixed deposits offer guaranteed returns and maximum safety

- Liquid funds provide high liquidity with low risk

- Debt funds offer slightly higher returns with moderate risk

- Short-term investing should prioritize safety over returns

- A combination approach often works best

Which is best for short-term investment in India?

For short-term investments in India, liquid funds are best for liquidity and emergency needs, debt funds are suitable for 6–24 months with slightly higher returns, and fixed deposits are ideal if you want guaranteed returns. The right choice depends on your time horizon and liquidity needs.

Understanding the Three Options Clearly

1. Fixed Deposits (FDs)

Fixed deposits are one of the most traditional and widely used investment options.

Key Features

- Guaranteed returns

- Fixed tenure

- Very low risk

Advantages

- Predictable income

- No market volatility

- Simple and easy to understand

Limitations

- Premature withdrawal penalty

- Limited liquidity

- Returns may not beat inflation

2. Liquid Funds

Liquid funds are mutual funds that invest in short-term instruments.

Key Features

- High liquidity

- Low risk

- Slightly better returns than savings accounts

Advantages

- Quick withdrawal (usually within 24 hours)

- No lock-in

- Efficient for short-term parking

Ideal Duration

- 1 day to 6 months

3. Debt Mutual Funds

Debt funds invest in bonds, government securities, and corporate instruments.

Key Features

- Moderate returns

- Low to moderate risk

- Better flexibility than FDs

Advantages

- Potential for higher returns than FDs

- Suitable for short to medium duration

- Diversification

Ideal Duration

- 6 months to 3 years

Quick Comparison Table

| Feature | FD | Liquid Fund | Debt Fund |

|---|---|---|---|

| Returns | Fixed | Low | Moderate |

| Risk | Very low | Low | Moderate |

| Liquidity | Low | High | Medium |

| Flexibility | Low | High | Medium |

Best Option Based on Your Goal

Choosing the right option depends on your objective.

Goal-Based Recommendation

| Goal Type | Best Option |

|---|---|

| Emergency fund | Liquid fund |

| Parking money (few months) | Liquid fund |

| Short-term goal (6–12 months) | Debt fund |

| Guaranteed return need | FD |

When Should You Choose Fixed Deposits?

Ideal Scenarios

- Capital safety is your highest priority

- You want guaranteed returns

- You have a fixed time horizon

- You prefer predictable outcomes

FDs are best suited for conservative investors.

When Should You Choose Liquid Funds?

Ideal Scenarios

- Emergency funds

- Temporary parking of money

- Very short-duration investments

Liquid funds provide flexibility and quick access.

When Should You Choose Debt Funds?

Ideal Scenarios

- Investment horizon of 6–24 months

- Slightly higher return expectations

- Moderate risk tolerance

Debt funds provide a balance between return and safety.

Returns Comparison (2026 Expectations)

| Investment Type | Expected Return |

|---|---|

| Savings Account | 2.5–4% |

| Fixed Deposit | 6–7.5% |

| Liquid Fund | 5–6.5% |

| Debt Fund | 6–8% |

Key Insight

Higher returns usually come with slightly higher risk.

Real-Life Allocation Examples

₹1 Lakh Portfolio

| Type | Allocation | Amount |

|---|---|---|

| FD | 50% | ₹50,000 |

| Liquid Fund | 30% | ₹30,000 |

| Debt Fund | 20% | ₹20,000 |

₹5 Lakh Portfolio

| Type | Allocation | Amount |

|---|---|---|

| FD | 40% | ₹2,00,000 |

| Liquid Fund | 30% | ₹1,50,000 |

| Debt Fund | 30% | ₹1,50,000 |

₹10 Lakh Portfolio

| Type | Allocation | Amount |

|---|---|---|

| FD | 35% | ₹3,50,000 |

| Liquid Fund | 35% | ₹3,50,000 |

| Debt Fund | 30% | ₹3,00,000 |

Interest Rate Impact (Important Insight)

Interest rates affect different instruments differently.

Impact Comparison

| Scenario | FD | Debt Fund |

|---|---|---|

| Interest rates rise | No impact | Prices may fall |

| Interest rates fall | No impact | Prices may rise |

Key Insight

Debt funds are sensitive to interest rate changes, while FDs are not.

Taxation Comparison

| Investment | Tax Treatment |

|---|---|

| FD | As per income slab |

| Liquid Fund | As per income slab |

| Debt Fund | As per income slab |

Risk Comparison

| Risk Type | FD | Liquid Fund | Debt Fund |

|---|---|---|---|

| Credit Risk | No | Low | Moderate |

| Interest Rate Risk | No | Low | Medium |

| Liquidity Risk | Medium | Low | Medium |

Quick Rule of Thumb

- 0–6 months → Liquid funds

- 6–24 months → Debt funds

- Need guaranteed returns → FD

How to Decide the Right Option (Step-by-Step Framework)

Choosing between FD, liquid funds, and debt funds can be confusing.

Use this simple framework:

Step 1: Identify Time Horizon

- Less than 6 months → Liquid fund

- 6 to 24 months → Debt fund

- Fixed duration → FD

Step 2: Check Liquidity Needs

- Need instant access → Liquid fund

- Can wait → Debt fund

- No liquidity needed → FD

Step 3: Understand Risk Tolerance

- Very low risk → FD

- Low risk → Liquid fund

- Moderate risk → Debt fund

Step 4: Define Purpose

- Emergency fund → Liquid fund

- Short-term goal → Debt fund

- Guaranteed returns → FD

Key Insight

The right investment depends on your situation, not just returns.

Real-Life Scenario: Choosing the Right Option

Let’s simplify this with practical examples.

Scenario 1: Emergency Fund (₹2 Lakh)

- Requirement: Immediate access

- Best Option: Liquid fund

Scenario 2: Vacation in 1 Year (₹3 Lakh)

- Requirement: Safety + moderate returns

- Best Option: Debt fund

Scenario 3: Fixed Goal After 2 Years (₹5 Lakh)

- Requirement: Guaranteed return

- Best Option: FD

Key Insight

Different goals require different instruments.

There is no single “best” option.

Common Mistakes Investors Make

- Chasing higher returns

- Ignoring liquidity

- Using equity for short-term goals

- Locking money without planning

To reduce risk, refer to How to Reduce Risk in Mutual Fund Investing (2026 Guide).

When NOT to Use Debt Funds

Debt funds are not suitable when:

- Investment horizon is less than 3 months

- You need emergency access

- You have very low risk tolerance

Advanced Insight: Ladder Strategy

Instead of choosing one option, combine all three.

Ladder Approach

| Duration | Instrument |

|---|---|

| 0–3 months | Liquid fund |

| 3–12 months | Debt fund |

| 1–3 years | FD |

Why This Works

- Improves liquidity

- Balances returns

- Reduces risk

How to Build a Smart Short-Term Portfolio

A well-balanced strategy is essential.

Suggested Approach

- Emergency fund → Liquid funds

- Short-term goals → Debt funds

- Safety needs → FDs

To understand allocation, refer to Mutual Fund Portfolio Allocation Strategy (Equity vs Debt vs Hybrid – 2026 Guide).

For low-risk strategies, refer to Best Low-Risk Mutual Funds Strategy in India (2026 Guide).

For short-term planning, refer to How to Choose Mutual Funds for Short-Term Goals (1–3 Years Investment Strategy 2026 Guide).

Advanced Insight: Behavior Matters

Successful short-term investing depends on:

- Planning

- Liquidity management

- Risk control

It is not about maximizing returns.

It is about protecting capital.

Conclusion

Choosing between fixed deposits, liquid funds, and debt funds is not about selecting the highest return option.

It is about:

- Matching investment with your goal

- Prioritizing safety and liquidity

- Maintaining discipline

Final Verdict

- FD = Safety

- Liquid Fund = Liquidity

- Debt Fund = Balance

Final Thought

Short-term investing is about protecting your money while keeping it accessible.

Frequently Asked Questions (FAQs)

1. Which is safest: FD, liquid fund, or debt fund?

FD is the safest.

2. Are liquid funds better than savings accounts?

Yes, generally.

3. Can debt funds give negative returns?

Yes, in certain cases.

4. Should I use equity for short-term goals?

No.

5. Which is best for emergency funds?

Liquid funds.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply