By Ashok Prasad, Founder, Niyyam

Published: March 2026

Building a ₹1 crore portfolio is one of the most common financial goals for Indian investors.

It is not just about money. It represents:

- Financial independence

- Security for your family

- Confidence to handle future goals

However, many investors believe that reaching ₹1 crore requires:

- High income

- Perfect market timing

- Aggressive risk-taking

This belief is incorrect.

In reality, wealth creation is a result of discipline, consistency, and a structured investment approach.

Even an average investor can build ₹1 crore using mutual funds by following a clear strategy.

💡 Key Takeaways

- ₹1 Crore is Achievable: You don’t need large capital — consistency matters more than amount.

- Compounding is the Real Driver: Time plays a bigger role than returns.

- Asset Allocation is Crucial: The right mix of equity and debt reduces risk and improves stability.

- SIP is the Most Practical Approach: It removes the need for market timing.

- Discipline Beats Intelligence: Staying invested matters more than selecting the “perfect” fund.

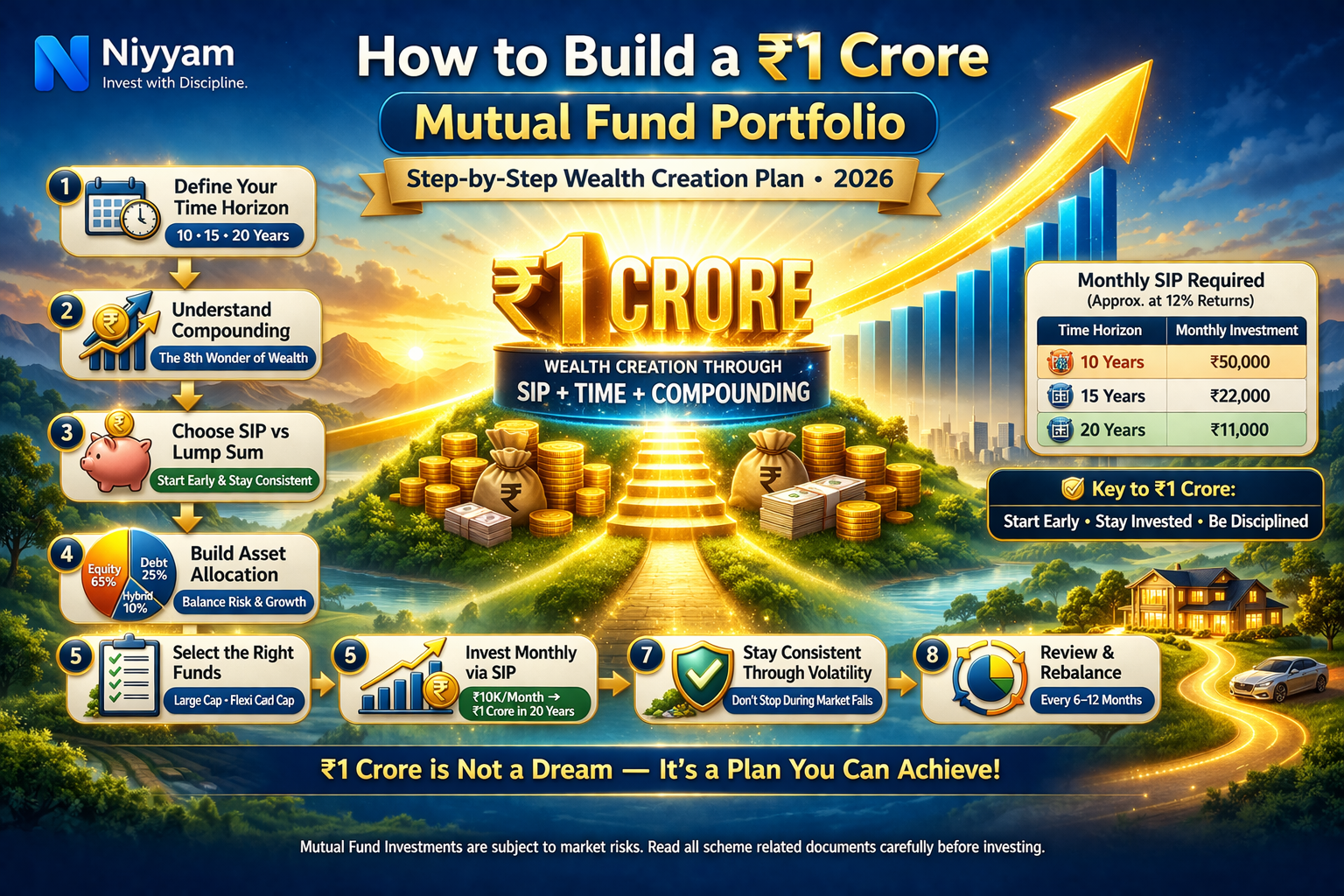

Step 1: Define Your Target Timeline

Before investing, clarity is essential.

Ask Yourself:

- When do I want ₹1 crore?

- Is this for retirement, a house, or long-term wealth?

Example Timelines:

- 10 years → Requires higher investment

- 15 years → Moderate effort

- 20 years → Easier through compounding

Important Insight:

- Time reduces risk and increases the probability of success

Refer:

How to Choose the Right SIP Duration in Mutual Funds (2026 Guide for Maximum Returns)

Step 2: Understand Compounding in Practical Terms

Compounding is not just a concept — it is the foundation of wealth creation.

Example:

If you invest ₹10,000 per month:

- 10 years → ~₹23 lakh

- 15 years → ~₹50 lakh

- 20 years → ~₹1 crore

Key Insight:

- The first 10 years build habit, the next 10 years build wealth

Refer:

How SIP Builds Wealth Through Compounding (With Simple Examples)

Step 3: Choose the Right Investment Strategy

SIP (Recommended)

- Best for salaried individuals

- Reduces volatility impact

- Builds discipline

Lump Sum

- Suitable for bonuses, inheritance

- Should be invested gradually

Smart Approach:

- Combine both if possible

Important Insight:

- Consistency is more powerful than timing the market

Refer:

SIP vs Lump Sum: Which Investment Strategy Is Better for Beginners?

Step 4: Build Strong Asset Allocation

Asset allocation determines long-term success.

Example Allocation:

- 65% Equity (growth)

- 25% Debt (stability)

- 10% Hybrid/Flexibility

Why This Works:

- Equity provides growth

- Debt reduces volatility

- Hybrid adds balance

Key Insight:

- Asset allocation drives the majority of portfolio performance

Refer:

Mutual Fund Portfolio Allocation Strategy (Equity vs Debt vs Hybrid – 2026 Guide)

Step 5: Select Fund Categories (Not Just Funds)

Ideal Structure:

- Large Cap → Stability

- Flexi Cap → Balance

- Mid Cap → Growth

- Debt Fund → Safety

Avoid selecting too many funds.

Important Insight:

- A simple portfolio performs better than a complex one

Refer:

Types of Mutual Funds in India: Equity, Debt, and Hybrid Explained

Step 6: Calculate Monthly Investment Requirement

Approximation (12% return):

| Time Horizon | Monthly SIP |

|---|---|

| 10 years | ₹50,000 |

| 15 years | ₹22,000 |

| 20 years | ₹11,000 |

Key Learning:

- Starting early reduces financial pressure

Important Insight:

- Delay is more costly than low returns

Step 7: Stay Consistent During Market Volatility

This is the most difficult step.

Common Investor Behavior:

- Stops SIP during market fall

- Withdraws due to fear

- Switches funds frequently

Correct Behavior:

- Continue investing

- Use volatility as an opportunity

Key Insight:

- Market downturns are wealth-building phases, not threats

Refer:

Why Most SIP Investors Fail to Build Wealth (And How to Avoid It in 2026)

Step 8: Review and Rebalance Your Portfolio

What to Do:

- Review every 6–12 months

- Adjust asset allocation

What Not to Do:

- React to short-term market movement

- Exit based on temporary underperformance

Important Insight:

- Review improves performance; overreaction destroys it

Refer:

How to Rebalance Your Mutual Fund Portfolio (When, Why & How – 2026 Guide)

Mini Case Study

Investor A

- Invests ₹10,000/month

- Stops SIP during a crash

- Changes funds frequently

Investor B

- Invests ₹10,000/month

- Continues SIP in all market conditions

- Stays disciplined

After 20 Years:

- Investor A → ₹65 lakh

- Investor B → ₹1+ crore

Key Insight:

- Discipline multiplies wealth; inconsistency destroys it

Common Mistakes to Avoid

- Trying to time the market

- Over-diversifying

- Ignoring asset allocation

- Stopping SIPs

Refer:

How Not to Choose a Mutual Fund: 7 Critical Mistakes Investors Must Avoid (2026 Guide)

Quick Rule of Thumb

To reach ₹1 crore:

- Start early

- Invest regularly

- Stay invested

- Avoid emotional decisions

Golden Rule:

- Wealth creation is a process, not an event

Frequently Asked Questions (FAQs)

1. Can I build ₹1 crore with SIP?

Yes, with consistency and time.

2. What return should I expect?

10–12% for long-term equity investing.

3. Is ₹10,000 SIP enough?

Yes, if invested for 20+ years.

4. Is a lump sum better than SIP?

SIP is safer for most investors.

5. What is the biggest mistake?

Stopping investments during a market fall.

6. How often should I review?

Every 6–12 months.

Final Thought

₹1 crore is not achieved by luck.

It is achieved by discipline.

Most investors fail not because they lack money,

But because they lack consistency.

If you start early, stay disciplined, and follow a structured plan,

₹1 crore becomes a predictable outcome — not a dream.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply