By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

Most investors believe that building wealth requires:

- Multiple mutual funds

- Complex strategies

- Frequent buying and selling

But in reality, simplicity often outperforms complexity.

Many investors today struggle with:

- Too many funds

- Portfolio overlap

- Confusion in tracking investments

If this sounds familiar, you are not alone.

The solution is surprisingly simple:

A well-structured 3-fund portfolio

Instead of managing 8–10 funds, you can create a powerful, diversified portfolio using just 3 mutual funds.

So the real question is:

Can just 3 funds really build long-term wealth effectively?

The answer is yes — if structured correctly.

Direct Answer

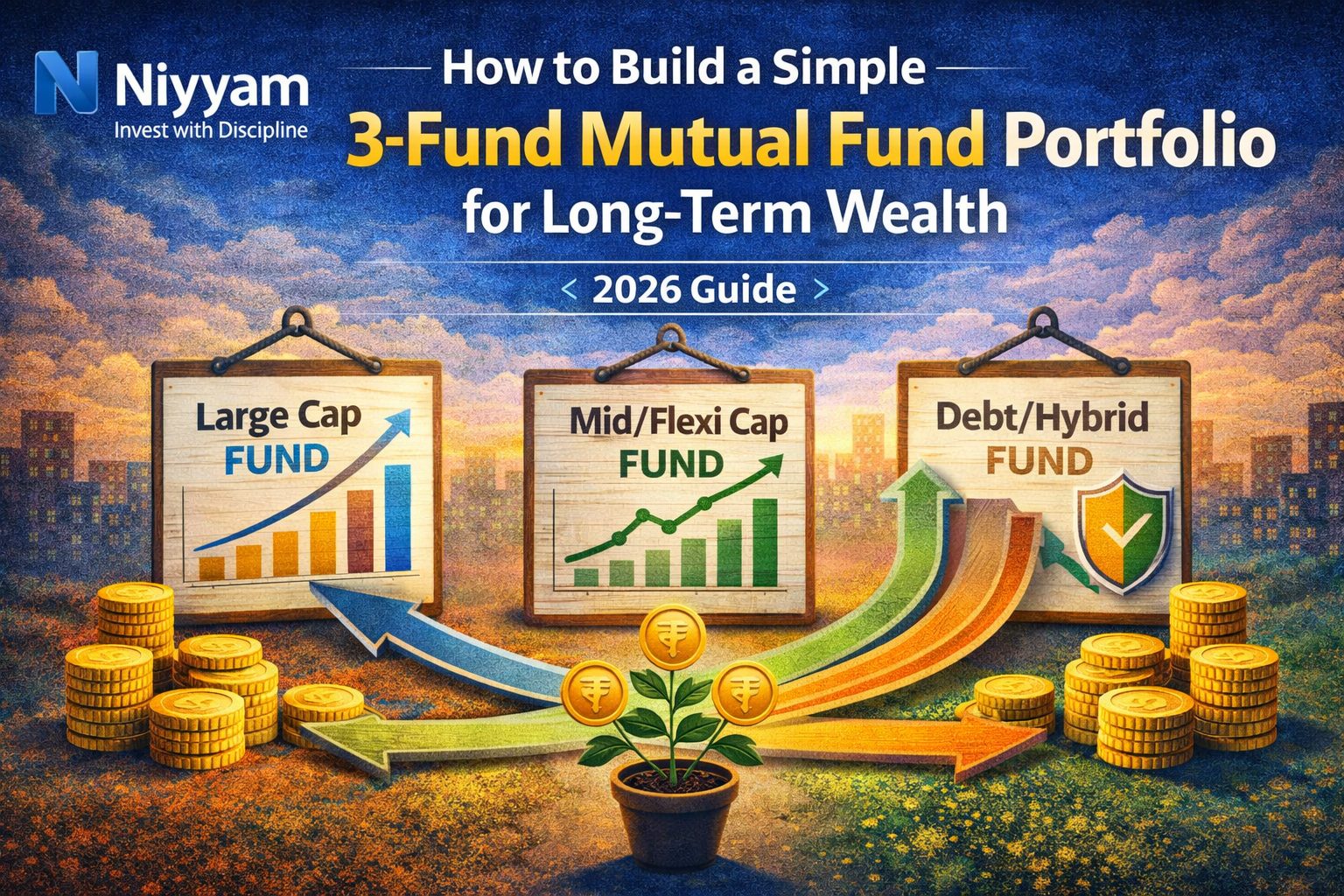

A 3-fund mutual fund portfolio consists of one large-cap fund, one mid-cap (or flexi-cap) fund, and one debt or hybrid fund. This structure provides diversification, growth, and stability for long-term wealth creation.

- Large Cap → Stability

- Mid/Flexi Cap → Growth

- Debt/Hybrid → Risk balance

💡 Key Takeaways

- 3 funds are sufficient for most investors

- Simple portfolios outperform cluttered portfolios

- Asset allocation matters more than fund count

- Avoid duplication and overlap

- Consistency drives long-term returns

- Periodic rebalancing is essential

- Simplicity improves discipline

What is a 3-Fund Portfolio?

A 3-fund portfolio is a minimal yet complete investment structure.

| Fund Type | Role | Objective |

|---|---|---|

| Large Cap | Stability | Protect capital |

| Mid/Flexi Cap | Growth | Wealth creation |

| Debt/Hybrid | Balance | Reduce volatility |

- It covers all essential market segments without complexity

Why 3 Funds Are Enough

| Reason | Explanation |

|---|---|

| Diversification | Covers equity + debt |

| Simplicity | Easy to manage |

| Efficiency | No duplication |

Many investors unnecessarily add more funds, which leads to inefficiency. This issue is explained in How to Consolidate Multiple Mutual Funds into a Clean Portfolio (2026 Guide).

Ideal Allocation in a 3-Fund Portfolio

| Category | Allocation |

|---|---|

| Large Cap | 40–50% |

| Mid/Flexi Cap | 30–40% |

| Debt/Hybrid | 10–30% |

- Allocation should match your risk profile

Allocation Based on Risk Profile

| Profile | Large Cap | Mid Cap | Debt |

|---|---|---|---|

| Aggressive | 40% | 50% | 10% |

| Moderate | 50% | 30% | 20% |

| Conservative | 60% | 20% | 20% |

Step-by-Step: Build Your 3-Fund Portfolio

Step 1: Choose a Large Cap Fund

| Criteria | What to Check |

|---|---|

| Consistency | 5–10 year performance |

| Expense ratio | Low cost |

| Portfolio quality | Blue-chip stocks |

- This is your portfolio’s foundation

Step 2: Choose a Growth Fund (Mid or Flexi Cap)

| Option | Benefit |

|---|---|

| Mid Cap | High growth potential |

| Flexi Cap | Dynamic allocation |

- This drives wealth creation

Step 3: Add Stability (Debt or Hybrid)

| Type | Role |

|---|---|

| Debt Fund | Stability |

| Hybrid Fund | Balanced exposure |

- Reduces portfolio volatility

Index Fund vs Active Fund (Important Decision)

| Factor | Index Fund | Active Fund |

|---|---|---|

| Cost | Low | Higher |

| Returns | Market-linked | Potentially higher |

| Risk | Lower | Moderate |

- You can combine both, depending on the strategy

Real-Life Portfolio Example

Moderate Investor

| Fund Type | Allocation | Monthly SIP |

|---|---|---|

| Large Cap | 50% | ₹5,000 |

| Mid Cap | 30% | ₹3,000 |

| Debt | 20% | ₹2,000 |

Outcome

- Balanced growth and stability

- Lower volatility

- Better long-term compounding

Before vs After Portfolio Simplification

| Scenario | Outcome |

|---|---|

| 10 funds | Confusion, overlap |

| 3 funds | Clarity, efficiency |

- Simplification improves performance

To understand overlap problems, refer to What is Portfolio Overlap in Mutual Funds & Why It Can Reduce Your Returns (2026 Guide).

Tax Efficiency in 3-Fund Portfolio

| Asset Type | Tax Rule |

|---|---|

| Equity | 10% LTCG above ₹1 lakh |

| Debt | As per tax slab |

- Long-term holding improves tax efficiency

Rebalancing Strategy (Very Important)

| Frequency | Action |

|---|---|

| Every 6–12 months | Review allocation |

| Market changes | Adjust weights |

| Goal change | Reallocate |

- Rebalancing maintains portfolio balance

SIP Strategy for 3-Fund Portfolio

| Fund | SIP Allocation |

|---|---|

| Large Cap | ₹5,000 |

| Mid Cap | ₹3,000 |

| Debt | ₹2,000 |

- Keep SIP simple and consistent

If you tend to create multiple SIPs unnecessarily, refer to Is It Good to Invest in the Same Mutual Fund via Multiple SIPs? (2026 Guide).

Common Mistakes Investors Make

- Adding too many funds

- Choosing similar categories

- Ignoring asset allocation

- Not reviewing the portfolio regularly

These issues often arise due to over-diversification, explained in How to Identify Over-Diversification in Mutual Funds (And Fix It in 2026).

Advanced Insight: Why 3 Funds Beat 10 Funds

| Factor | 3 Funds | 10 Funds |

|---|---|---|

| Clarity | High | Low |

| Overlap | Low | High |

| Tracking | Easy | Difficult |

| Efficiency | High | Low |

- More funds do not mean better returns

When Should You NOT Use the 3-Fund Strategy?

| Situation | Reason |

|---|---|

| Very high portfolio (>₹1 Cr) | Needs advanced allocation |

| Multiple financial goals | Requires segmentation |

Decision Framework (MOST IMPORTANT)

| Scenario | Action |

|---|---|

| Beginner | Start with 3 funds |

| Too many funds | Consolidate |

| Confused portfolio | Simplify |

Impact on Long-Term Wealth

| Strategy | Outcome |

|---|---|

| Simple 3-fund portfolio | Strong compounding |

| Complex portfolio | Average returns |

- Clarity leads to discipline → discipline leads to wealth

Frequently Asked Questions (FAQs)

Is a 3-fund portfolio enough?

Yes, for most investors.

Which funds should I choose?

Large cap, mid/flexi cap, and debt/hybrid.

Can 3 funds create wealth?

Yes, with discipline and long-term investing.

Is it better than multiple funds?

Yes, due to efficiency and clarity.

How often should I rebalance?

Once or twice a year.

Final Verdict

A 3-fund portfolio is one of the most effective strategies for long-term wealth creation.

- Simple to manage

- Balanced risk

- High efficiency

You don’t need more funds — you need the right structure.

Final Thought

Wealth creation does not come from complexity.

- It comes from discipline, patience, and simplicity

Start simple, stay consistent, and let compounding do the rest.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply