By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

Most mutual fund advice focuses on long-term investing.

But what if your goal is just 1 to 3 years away?

For example:

- Buying a car

- Planning a vacation

- Paying a down payment

- Building an emergency buffer

The challenge is:

How do you invest in mutual funds for short-term goals without taking unnecessary risk?

Because in the short term:

- Markets are unpredictable

- Equity can be volatile

- Wrong choices can lead to losses

Many investors make the mistake of chasing returns instead of protecting capital.

The truth is:

Short-term investing is not about maximizing returns. It is about minimizing risk while achieving your goal.

💡 Key Takeaways

- Capital protection should be the primary focus for 1–3 year goals

- Debt funds are generally the most suitable option

- Limited hybrid exposure can be used cautiously

- Equity funds are not ideal for short-term goals

- Liquidity and stability are more important than returns

- Proper fund selection reduces risk significantly

If you are new, it is important to understand what is a mutual fund and how it works, because that forms the base of your decision-making.

Why Short-Term Investing Is Different

Short-term investing behaves very differently from long-term investing.

Key Differences

- Less time to recover from losses

- Higher sensitivity to volatility

- Lower margin for error

In long-term investing:

- Time reduces risk

In short-term investing:

- Wrong decisions increase risk significantly

Expected Returns for 1–3 Years (Reality Check)

Before selecting funds, you must set realistic expectations.

Typical Return Range

- Liquid funds: 4% to 6%

- Ultra short duration funds: 5% to 6.5%

- Low duration funds: 6% to 7%

- Conservative hybrid funds: 6% to 8%

Important Insight

- Returns are lower because risk is controlled

- Trying to increase returns increases risk

If you want to understand broader expectations, refer to how much return can you expect from mutual funds in India.

Biggest Mistake Investors Make

Many investors:

- Invest in equity funds for short-term goals

- Expect quick, high returns

This is risky because:

- Markets can fall anytime

- Recovery may take years

Ideal Mutual Fund Types for Short-Term Goals

Debt Funds (Primary Choice)

Debt funds are the safest mutual fund category for short-term investing.

Advantages

- Lower volatility

- Predictable returns

- Better capital protection

Types of Debt Funds to Consider

- Liquid funds

- Ultra-short duration funds

- Low-duration funds

These are designed for:

- Short-term horizons

- Stability

Conservative Hybrid Funds (Limited Use)

- Small equity exposure

- Slightly higher returns than pure debt

- Moderate risk

Funds to Avoid

Avoid:

- Mid-cap funds

- Small-cap funds

- Sectoral funds

These carry high volatility and are not suitable.

Fund Selection Checklist (Very Important)

Before choosing any fund, check:

- Low volatility history

- Consistent performance

- Short portfolio duration

- High liquidity

- Low expense ratio

To understand cost impact, read what is expense ratio in mutual funds and how it affects your returns.

Step-by-Step Investment Strategy

Step 1: Define Your Goal

- Exact amount required

- Clear timeline

Step 2: Choose Asset Allocation

- 80%–100% in debt funds

- 0%–20% in conservative hybrid

Step 3: Decide Investment Mode

- Lump sum for immediate deployment

- SIP if investing gradually

To understand better, refer to SIP vs lump sum which is better for beginners.

Step 4: Monitor Periodically

- Review every 3–6 months

- Avoid frequent changes

Real-Life Scenario 1 (1-Year Goal)

Profile

- Goal: ₹3 lakh in 1 year

Strategy

- 100% liquid funds

Outcome

- Stable returns

- Minimal risk

Real-Life Scenario 2 (2-Year Goal)

Profile

- Goal: ₹5 lakh

Strategy

- Liquid + ultra-short duration funds

Outcome

- Better returns than a savings account

- Low volatility

Real-Life Scenario 3 (3-Year Goal)

Profile

- Goal: ₹10 lakh

Strategy

- 80% debt funds

- 20% conservative hybrid

Outcome

- Balanced return and stability

Risk Management Strategy

Avoid Equity Exposure

- Equity increases volatility

- Not suitable for short-term

Diversify Across Funds

- Use 2–3 funds

- Avoid concentration risk

Keep Emergency Fund Separate

- Do not mix goals

Stay Disciplined

- Avoid unnecessary changes

Taxation in Short-Term Investing

Debt Funds

- Gains are taxed as per the income slab

Hybrid Funds

- Tax depends on equity exposure

To understand clearly, refer to the mutual fund taxation in India explained.

Decision Framework (Quick Guide)

If your goal is:

- Less than 1 year → Avoid mutual funds

- 1–2 years → Liquid / ultra short funds

- 2–3 years → Low duration + hybrid mix

If your risk tolerance is:

- Low → 100% debt

- Moderate → Small hybrid allocation

If you need:

- Stability → Debt funds

- Slight growth → Hybrid funds

Common Mistakes to Avoid

Chasing High Returns

High return = high risk.

Ignoring Risk

Short-term investing is risk-sensitive.

Over-diversification

Too many funds reduce clarity.

Frequent Switching

Destroys stability.

No Clear Goal

Leads to poor decisions.

When Should You Avoid Mutual Funds?

Avoid mutual funds if:

- Your investment horizon is less than 1 year

- You need guaranteed returns

- You cannot tolerate any fluctuation

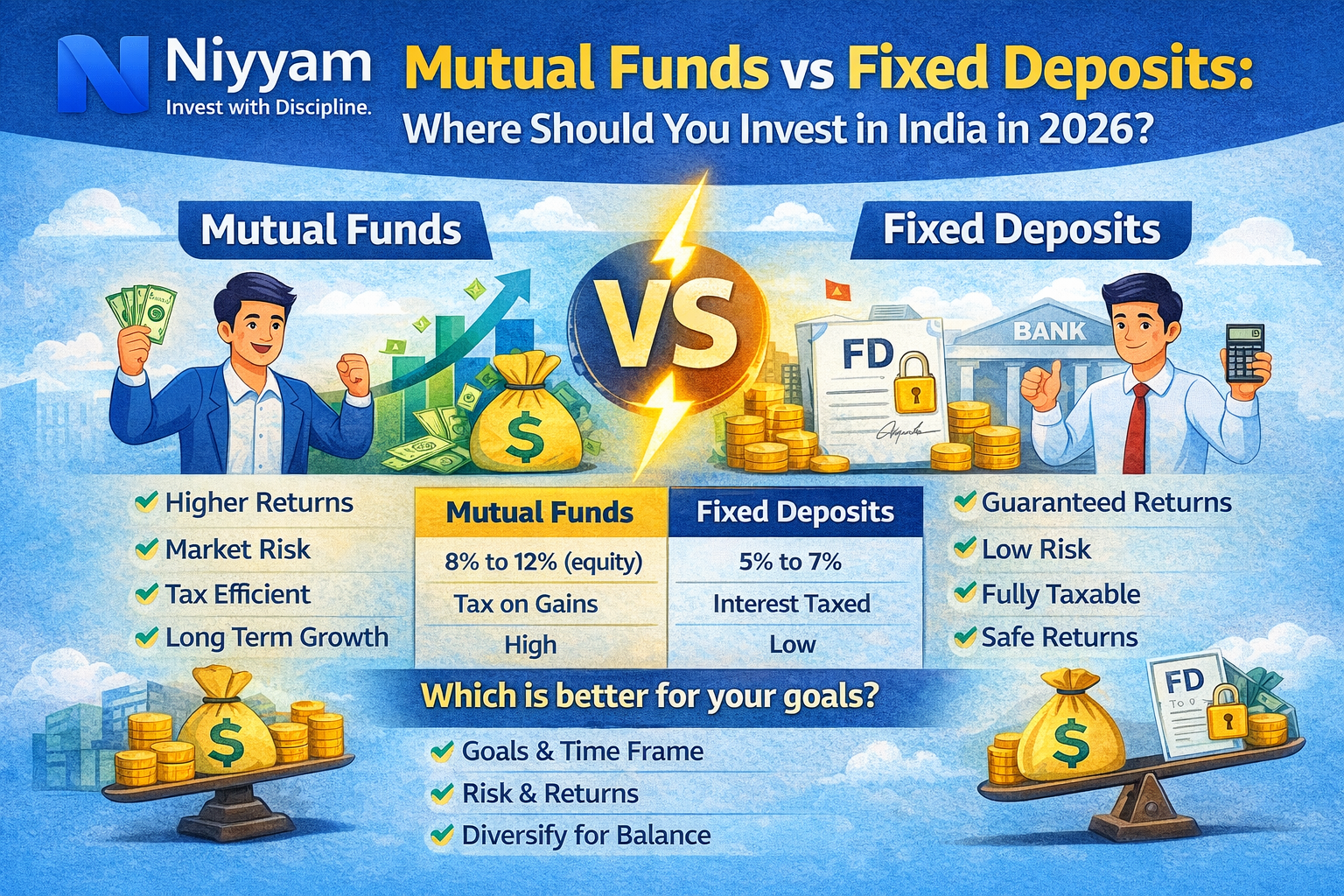

In such cases, you can consider fixed deposits.

You can compare options through mutual funds vs fixed deposits where should you invest in India.

{kind=link}

Advanced Insight: Balance Between Safety and Returns

Short-term investing is about balance:

- Too safe → low returns

- Too aggressive → risk of loss

The ideal approach is:

Controlled risk with reasonable return expectations

Frequently Asked Questions (FAQs)

Can I invest in equity funds for short-term goals?

Not recommended due to volatility.

Which mutual fund is safest?

Liquid and ultra short duration funds.

Can I use SIP?

Yes, but lump sum may also be effective.

Are returns guaranteed?

No, but risk is lower in debt funds.

How often should I review?

Every 3 to 6 months.

What if the market falls?

Debt funds are less affected than equity funds.

Final Thought

Short-term investing is not about chasing returns.

It is about:

- Protecting your capital

- Achieving your goal

- Avoiding unnecessary risk

If you stay disciplined and follow the right strategy:

You can achieve your short-term goals with confidence and stability.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply