By Ashok Prasad, Founder, Niyyam

Published: March 2026

Choosing a mutual fund is easy. Choosing the right mutual fund is where most investors fail.

With hundreds of mutual funds available in India, many investors rely on:

- Recent performance

- Popular recommendations

- Online rankings

But this approach often leads to:

- Wrong fund selection

- Poor long-term returns

- Unnecessary risk

The reality is simple:

Not all mutual funds are equal, even within the same category.

To invest wisely, you need a structured and practical comparison framework.

In this guide, you will learn:

- The 5 most important metrics to compare mutual funds

- How to interpret these metrics correctly

- A real example of fund comparison

- Common mistakes investors must avoid

- A step-by-step framework you can apply immediately

Why Comparing Mutual Funds is Critical

Many investors assume:

- All large-cap funds perform similarly

- Higher returns mean better funds

- SIP investments will average out the differences

This is not true.

Even within the same category:

- Some funds take higher risks

- Some charge higher expenses

- Some are inconsistent performers

Important Insight:

If you don’t compare mutual funds properly, you are investing blindly.

The 5 Key Metrics to Compare Mutual Funds

1. Returns (Focus on Consistency, Not Just High Numbers)

Returns are the most visible metric, but also the most misunderstood.

Instead of only looking at:

- 1-year returns

You should compare:

- 3-year returns

- 5-year returns

- Performance across different market conditions

Important Point:

Consistent performance is more important than occasional high returns.

A fund that delivers:

- 12% consistently is better than

- 18% one year and 5% the next

What to check:

- Does the fund beat its benchmark regularly?

- Is performance stable across time periods?

To understand how returns actually work, read

“How Mutual Funds Generate Returns for Investors (With Simple Examples)”

2. Expense Ratio (The Silent Wealth Destroyer)

The expense ratio is the annual fee charged by the mutual fund.

It may look small, but over time, it has a huge impact on your wealth.

For example:

- A 1% difference over 20 years can reduce returns by lakhs

Important Point:

Lower expense ratio = higher returns for you

Always compare:

- Expense ratios within the same category

- Direct vs regular plans

To understand this in depth, read

“What is Expense Ratio in Mutual Funds? How It Affects Your Returns (2026 Guide)”

3. Risk Measures (Understanding Volatility)

Returns without risk analysis are misleading.

Key risk indicators:

- Standard deviation (volatility)

- Beta (market sensitivity)

- Sharpe ratio (risk-adjusted return)

Sharpe Ratio is especially important:

- It tells you how much return you get per unit of risk

Important Insight:

A fund with better risk-adjusted returns is superior to a high-return but high-risk fund.

4. Fund Manager & Investment Strategy

A mutual fund’s performance depends heavily on the fund manager.

Things to check:

- Experience of the fund manager

- Tenure managing the fund

- Investment style

Also consider:

- Is the strategy consistent?

- Does the fund frequently change its approach?

Important Point:

Frequent changes in fund management can impact performance stability.

5. Portfolio Composition (Where Your Money Goes)

Always check what the fund invests in.

Look at:

- Top holdings

- Sector allocation

- Market cap allocation

Example:

- A large-cap fund should primarily invest in large-cap stocks

- Over-concentration in one sector increases risk

Important Insight:

Well-diversified portfolios reduce risk and improve stability.

To learn how to build a strong portfolio, read

“How to Build a Mutual Fund Portfolio for Long-Term Wealth Creation (2026 Guide)”

{kind=link}

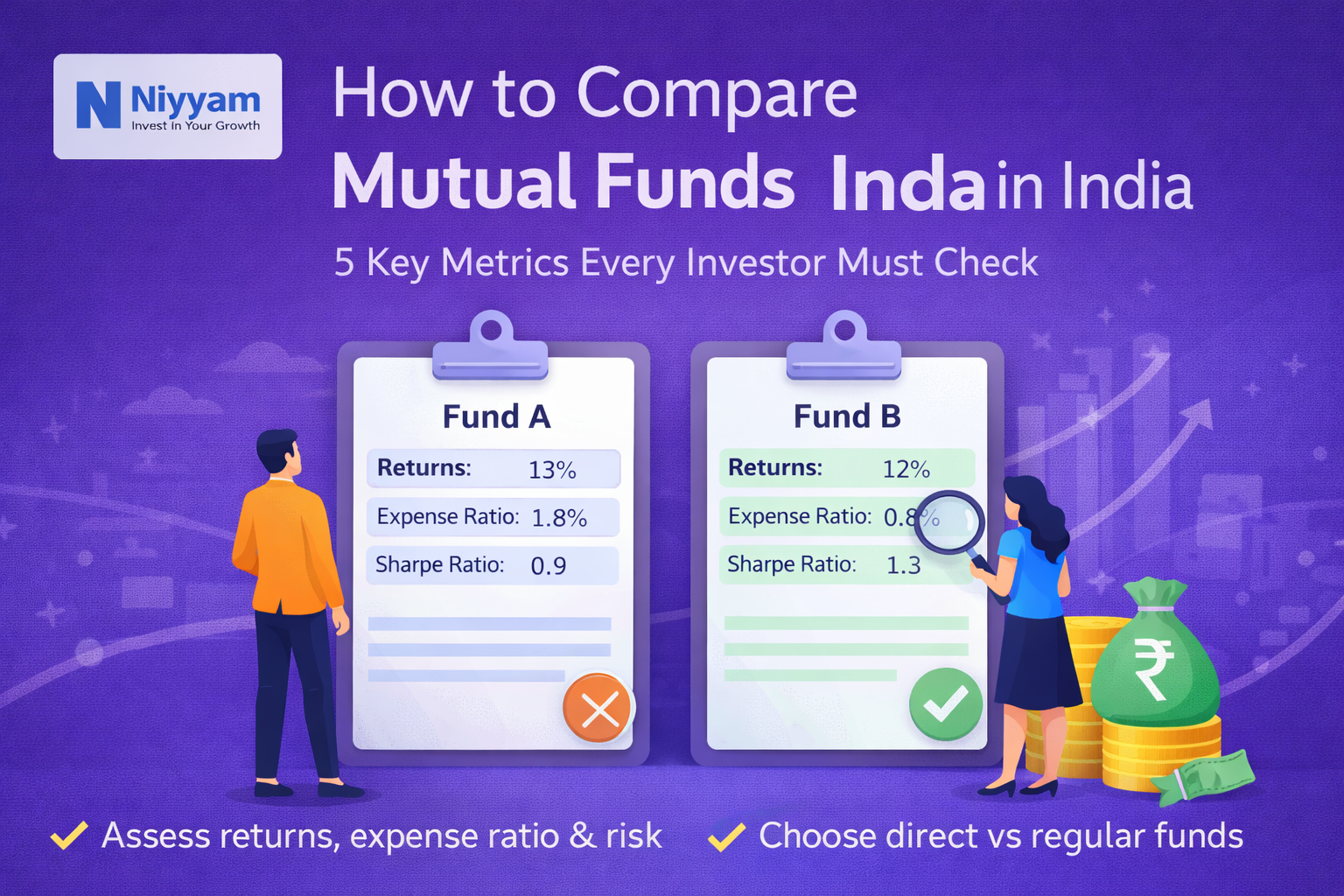

Real Example: Comparing Two Mutual Funds

Let’s compare two hypothetical large-cap funds:

Fund A

- 5Y Return: 13%

- Expense Ratio: 1.8%

- Sharpe Ratio: 0.9

- High volatility

Fund B

- 5Y Return: 12%

- Expense Ratio: 0.8%

- Sharpe Ratio: 1.3

- Stable performance

Which is better?

Most investors will choose Fund A because of higher returns.

But the better choice is Fund B, because:

- Lower cost

- Better risk-adjusted returns

- More consistent performance

Important Insight:

The best fund is not the one with the highest returns, but the one with a better balance of return, cost, and risk.

Step-by-Step Framework to Compare Mutual Funds

Use this simple process:

- Step 1: Shortlist 3–5 funds in the same category

- Step 2: Compare 3-year and 5-year returns

- Step 3: Check expense ratio

- Step 4: Compare the Sharpe ratio

- Step 5: Analyze portfolio allocation

Then choose the fund that offers:

- Consistency

- Reasonable cost

- Balanced risk

Common Mistakes to Avoid

Avoid these common errors:

- Choosing funds based only on recent returns

- Ignoring expense ratio

- Not checking risk metrics

- Investing in too many funds

- Following random advice

Important Point:

Avoiding mistakes is more important than finding the “perfect” fund.

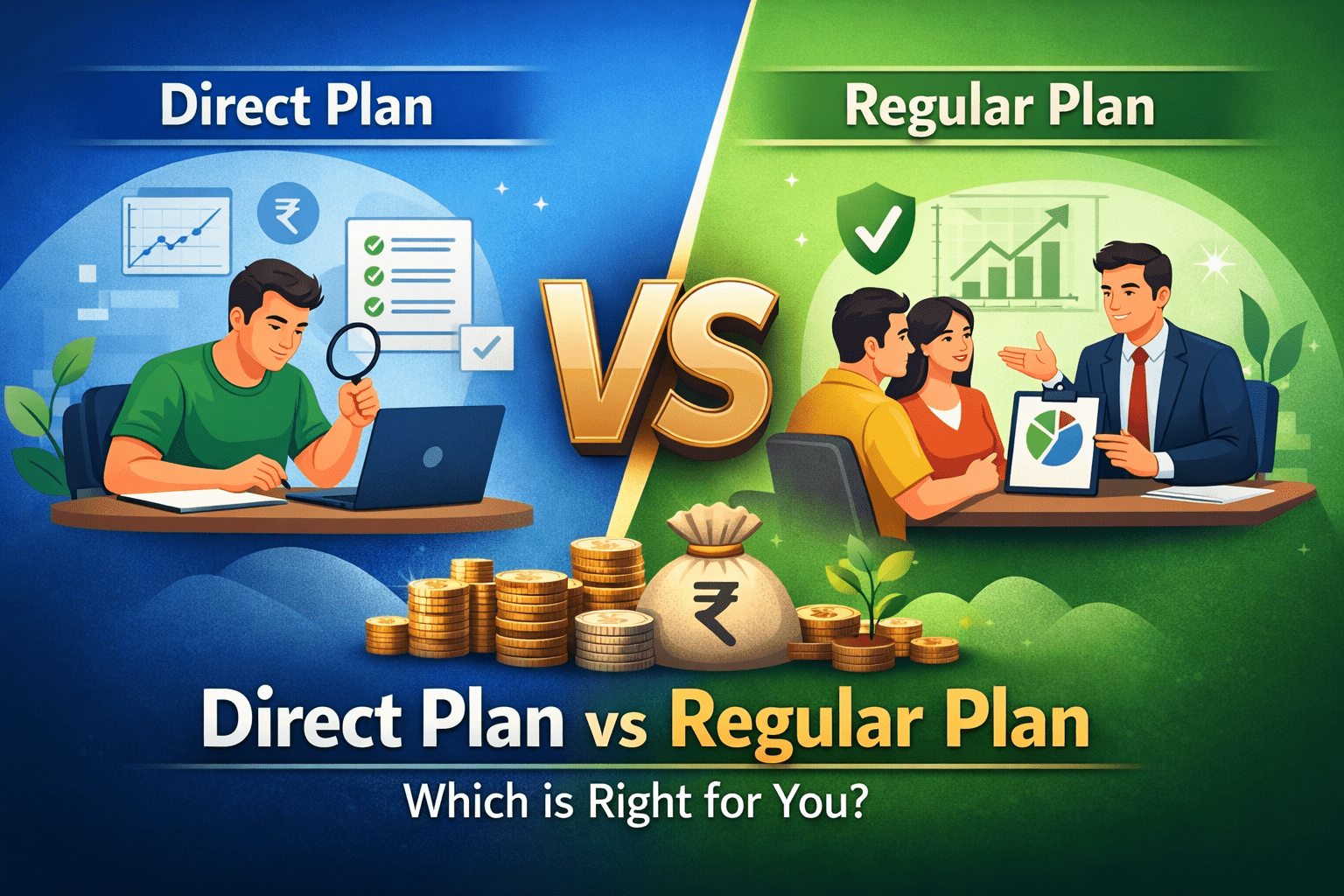

Direct vs Regular Funds: A Critical Comparison

Always compare:

- Direct plans → lower expense ratio

- Regular plans → higher costs due to commissions

Over long periods:

- Direct plans can generate significantly higher returns

To understand this better, read

“Direct vs Regular Mutual Funds: Which Should You Choose? (2026 Guide for Investors)”

{kind=link}

How SIP Investors Should Compare Funds

If you invest through SIP:

Focus on:

- Long-term consistency

- Risk-adjusted returns

- Expense ratio

Avoid focusing on:

- Short-term performance

To understand how SIP builds wealth, read

“How SIP Builds Wealth Through Compounding (With Simple Examples)”

Advanced Insight: Alpha (Bonus Metric)

Alpha measures how much extra return a fund generates over its benchmark.

- Positive alpha → fund is outperforming

- Negative alpha → underperformance

Important Insight:

Funds with consistent positive alpha are strong performers.

Final Checklist Before Investing

Before selecting a mutual fund, ensure:

- The fund shows consistent long-term performance

- The expense ratio is competitive

- Risk level matches your profile

- Portfolio is diversified

- The fund manager has a stable track record

If all these are satisfied, you are making a well-informed decision.

Conclusion

Comparing mutual funds is not complicated if you focus on the right metrics.

Instead of chasing returns, focus on:

- Consistency

- Cost efficiency

- Risk management

Because in investing:

The right fund is not the one that performs best today, but the one that helps you stay invested for the long term.

To deepen your understanding, read

“How to Choose the Right Mutual Fund in India (A Beginner’s Practical Guide)”

Frequently Asked Questions (FAQs)

1. How do I compare mutual funds in India?

Compare mutual funds based on returns, expense ratio, risk metrics, fund manager, and portfolio composition.

2. Is a higher return always better?

No. A fund with consistent and risk-adjusted returns is better than a high but volatile return fund.

3. What is the most important metric in mutual funds?

There is no single metric. A combination of consistency, cost, and risk-adjusted return matters.

4. Should I choose direct or regular mutual funds?

Direct funds are generally better due to lower expense ratios and higher long-term returns.

5. How many mutual funds should I compare before investing?

Shortlist 3–5 funds in the same category for effective comparison.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply