By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

When it comes to mutual fund investing, most people focus on:

- Which fund to choose

- What return to expect

- When to invest

But the most powerful factor is often ignored:

How long do you stay invested?

A simple SIP can create very different outcomes depending on time.

- 5 years → limited growth

- 10 years → noticeable wealth

- 20 years → transformational wealth

💡 Key Takeaways

- Time is the most powerful driver of wealth creation

- SIP returns grow exponentially over long durations

- Compounding becomes dominant after 10+ years

- Short-term investing limits wealth potential

- Consistency matters more than investment amount

- Staying invested is critical for success

If you are new, it is important to understand what is SIP in mutual funds and how it works, because SIP is the foundation of disciplined investing.

This guide will help you clearly understand:

- How time changes your wealth

- Why longer duration matter

- How to use SIP effectively

The Power of Time in SIP Investing

SIP works on two key principles:

- Rupee cost averaging

- Compounding

In early years:

- Cost averaging plays a role

In later years:

- Compounding becomes the main driver

To understand this clearly, you should read how SIP builds wealth through compounding.

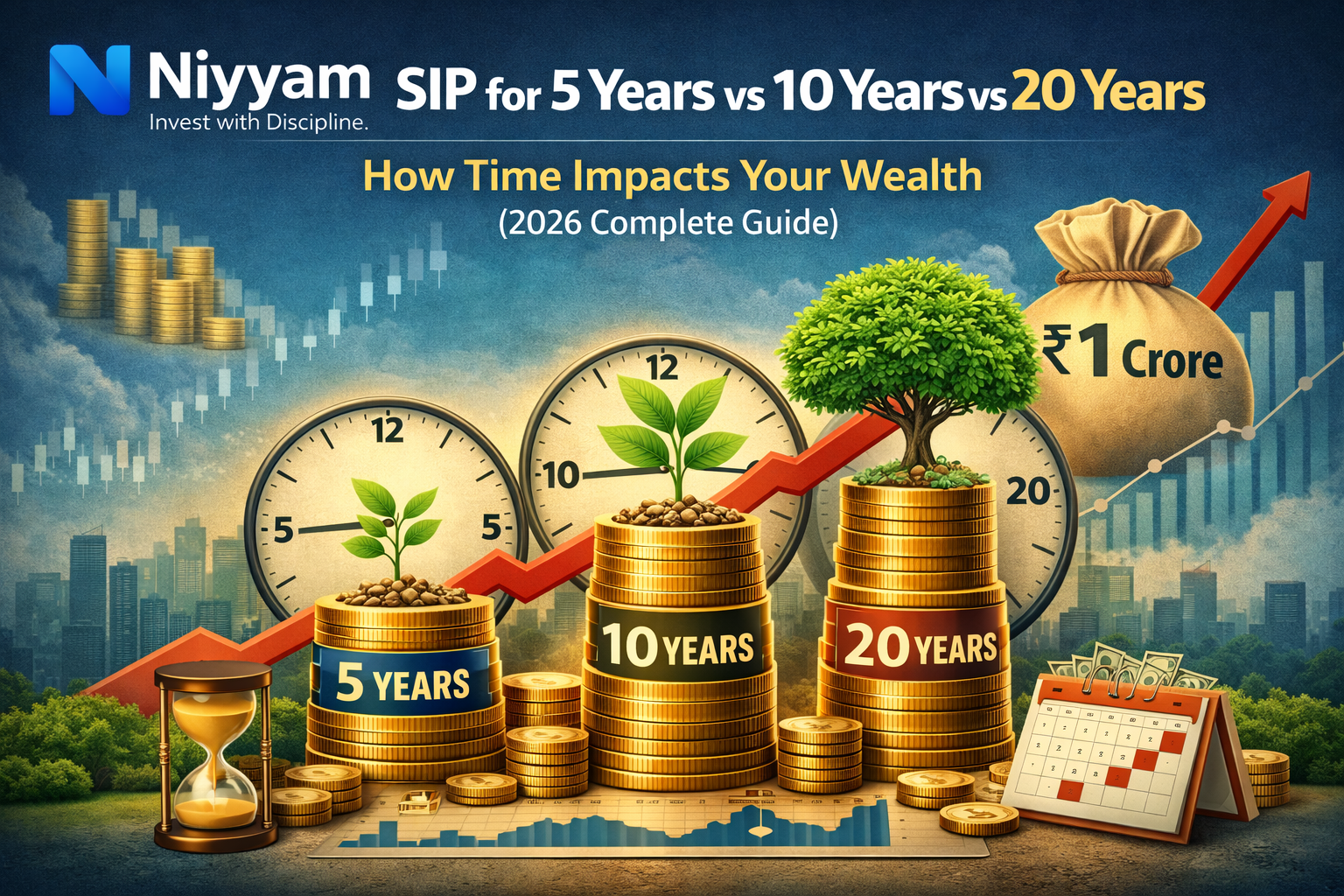

SIP Comparison: 5 vs 10 vs 20 Years

Let’s take a practical example:

- SIP: ₹10,000/month

- Return: 12%

SIP for 5 Years

- Total investment: ₹6 lakh

- Estimated value: ~₹8.4 lakh

- Gain: ~₹2.4 lakh

SIP for 10 Years

- Total investment: ₹12 lakh

- Estimated value: ~₹23 lakh

- Gain: ~₹11 lakh

SIP for 20 Years

- Total investment: ₹24 lakh

- Estimated value: ~₹1.2 crore

- Gain: ~₹96 lakh

Key Insight

- Investment increases 4x (₹6L → ₹24L)

- Wealth increases ~14x (₹8.4L → ₹1.2Cr)

This is the real power of time.

Why Most Wealth Is Created in the Last 5–10 Years

This is the most important concept.

Early Years (0–5 years)

- Slow growth

- Limited compounding

Middle Years (5–10 years)

- Compounding starts

- Growth improves

Later Years (10–20 years)

- Compounding accelerates

- Wealth grows exponentially

Example Insight

- First 10 years → ₹23 lakh

- Next 10 years → ₹1.2 crore

More wealth is created in later years than in earlier years.

Real-Life Case Study (Same SIP, Different Duration)

Investor A (5 Years)

- Value: ₹8.4 lakh

Investor B (10 Years)

- Value: ₹23 lakh

Investor C (20 Years)

- Value: ₹1.2 crore

Lesson

Time creates the biggest difference—not fund selection.

Step-Up SIP Case Study (Powerful Strategy)

Scenario

- Starting SIP: ₹10,000

- Increase: 10% annually

- Duration: 20 years

Outcome

- Significantly higher corpus than fixed SIP

- Faster wealth creation

Insight

Increasing SIP over time:

- Boosts compounding

- Accelerates wealth

What Happens If You Stop SIP Early?

Many investors stop SIP due to:

- Low initial returns

- Market fear

- Impatience

This reduces wealth significantly.

To understand the impact, read what happens when you stop SIP complete impact explained.

{kind=link}

Role of Market Cycles

Markets go through:

- Bull phases

- Bear phases

Short-term investors:

- Get affected

Long-term investors:

- Benefit

To understand this, refer to SIP in a bear market vs bull market.

Time vs Amount: Which Matters More?

Scenario Comparison

- ₹5,000 SIP for 20 years

- ₹15,000 SIP for 5 years

In many cases:

Longer duration creates more wealth than a higher amount invested for a shorter time.

How to Maximize SIP Returns

Start Early

- More time for compounding

Stay Consistent

- Avoid stopping SIP

Increase SIP Regularly

- Step-up strategy

Stay Invested During Market Falls

- Buy more units

You can learn how to invest during market crashes in mutual funds.

SIP Duration Strategy

1–5 Years

- Not ideal for wealth creation

- Suitable for short-term goals

5–10 Years

- Moderate wealth creation

- Some stability

10–20 Years

- Strong compounding

- Significant wealth

20+ Years

- Maximum wealth creation

- Financial independence possible

Practical Decision Framework

If your goal is:

- Short-term (1–3 years) → avoid equity SIP

- Medium-term (5–10 years) → balanced approach

- Long-term (10+ years) → equity SIP

If your priority is:

- Safety → shorter duration

- Growth → longer duration

Common Mistakes to Avoid

Stopping SIP Early

- Breaks compounding

Expecting Quick Results

- SIP requires patience

Ignoring Market Volatility

- Volatility is normal

Not Increasing SIP

- Limits growth

Frequent Fund Switching

- Reduces returns

Advanced Insight: Time Is a Multiplier

Think of SIP like this:

- Amount = fuel

- Time = engine

Without time:

- Growth remains limited

With time:

- Growth multiplies

Frequently Asked Questions (FAQs)

Is a 5-year SIP enough?

Not ideal for wealth creation.

Is a 10-year SIP good?

Yes, for moderate growth.

Is a 20-year SIP best?

Yes, for long-term wealth creation.

Can I stop SIP anytime?

Yes, but not recommended early.

What return can I expect?

10% to 12% over the long term.

Should I increase SIP?

Yes, it improves results significantly.

Final Thought

If you want to build wealth:

Focus on time, not timing.

- Start early

- Stay consistent

- Think long term

Because in investing:

Time is not just important—it is the biggest multiplier of wealth.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply