By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

One of the most common questions investors ask is:

“How much return can I expect from mutual funds?”

Many people start investing with expectations like:

- 15% to 20% guaranteed returns

- Fast wealth creation

- Consistent yearly gains

But when actual returns fluctuate, it leads to:

- Confusion

- Disappointment

- Poor financial decisions

The reality is simple:

Mutual fund returns are not fixed. They are market-linked and vary over time.

💡 Key Takeaways

- Mutual fund returns are market-linked and not guaranteed

- Equity funds offer higher returns with higher volatility

- Debt funds provide stability with lower returns

- Hybrid funds balance risk and return

- Time horizon is the most important factor in returns

- Realistic expectations prevent poor investment decisions

If you are new to investing, it is important to first understand what is a mutual fund and how it works, because returns are directly linked to how these investments function.

This guide will give you a clear, realistic, and practical understanding of what returns you can expect in India.

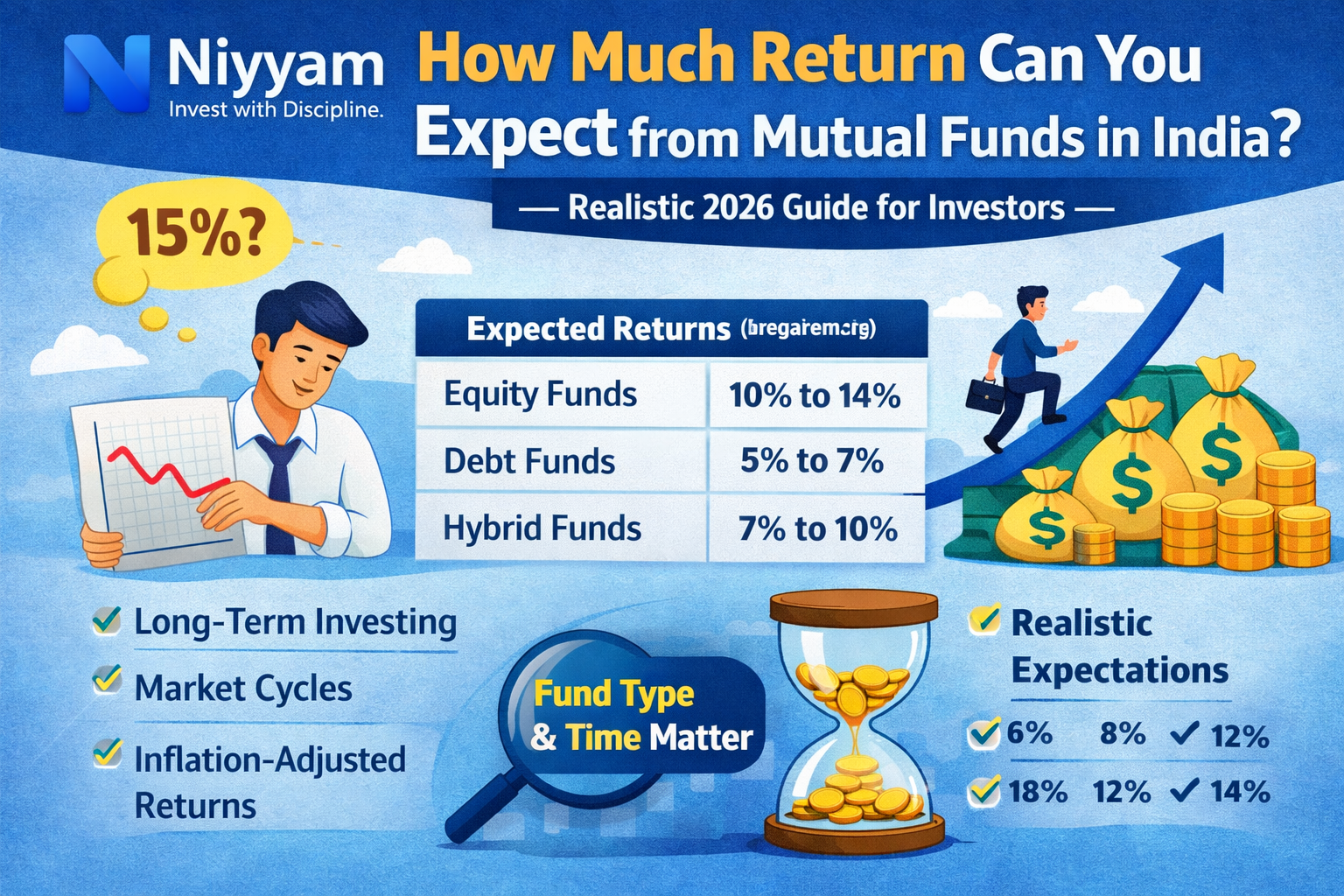

Average Returns from Mutual Funds in India

Let’s start with realistic benchmarks.

Equity Mutual Funds

- Expected return: 10% to 14% (long term)

- High short-term volatility

- Suitable for long-term wealth creation

Debt Mutual Funds

- Expected return: 5% to 7%

- Lower risk

- Suitable for stability and short-term goals

Hybrid Mutual Funds

- Expected return: 7% to 10%

- Balanced approach

- Moderate risk

To understand these categories in detail, you can explore types of mutual funds in India: equity, debt, and hybrid explained.

Category-Wise Return Expectations (Deeper View)

Large Cap Funds

- Expected return: 10% to 12%

- More stable

- Lower volatility

Mid Cap Funds

- Expected return: 12% to 15%

- Higher growth potential

- Moderate risk

Small Cap Funds

- Expected return: 14% to 18% (long term)

- High volatility

- Suitable only for long-term investors

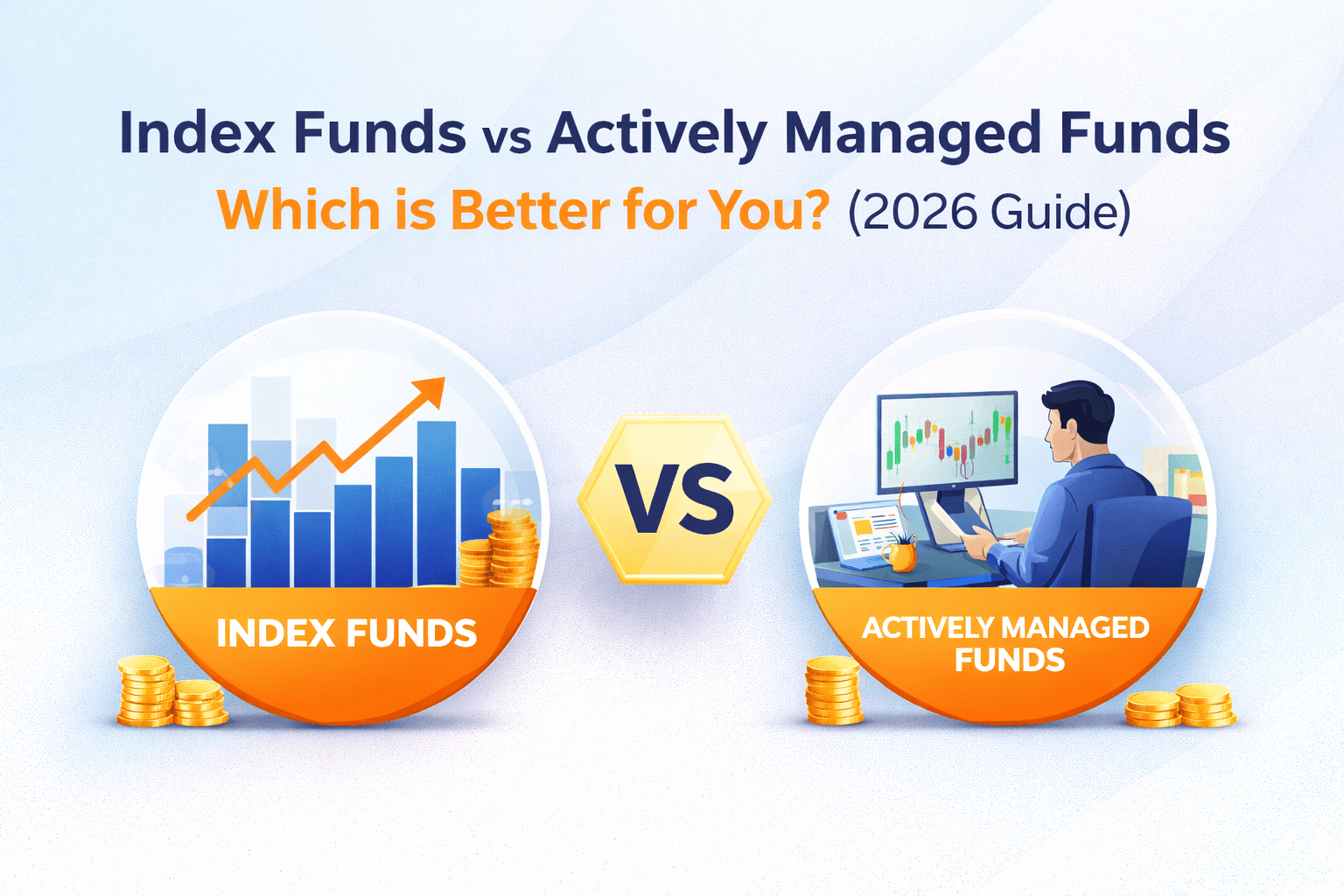

Index Funds

- Expected return: 10% to 12%

- Low cost

- Market-linked returns

To understand this better, you can read index funds vs actively managed funds, which explains how strategies impact returns.

{kind=link}

Returns Based on Investment Duration

1–3 Years

- Returns can be low or negative

- High unpredictability

3–5 Years

- Returns stabilize

- Better consistency

5–10 Years

- Strong probability of positive returns

- Compounding begins

10+ Years

- Wealth creation phase

- More reliable outcomes

To understand long-term impact, you should read how SIP builds wealth through compounding.

SIP vs Lump Sum Returns

SIP Investing

- Reduces market timing risk

- Benefits from cost averaging

- More stable outcomes

Lump Sum Investing

- Higher returns if invested at the right time

- Higher risk if timing is wrong

Practical Comparison

- SIP works better for:

- Regular investors

- Volatile markets

- Lump sum works better when:

- The market is undervalued

If you want clarity, you can explore SIP vs lump sum: which investment strategy is better for beginners.

Real-Life Case Study 1 (SIP Investor)

Scenario

- SIP: ₹10,000/month

- Duration: 10 years

- Average return: 12%

Outcome

- Total investment: ₹12 lakh

- Value: ~₹23 lakh

Real-Life Case Study 2 (Lump Sum Investor)

Scenario

- Investment: ₹10 lakh

- Duration: 10 years

- Return: 12%

Outcome

- Value: ~₹31 lakh

Insight

- A lump sum generates higher returns

- But requires correct timing

Inflation-Adjusted Returns (Very Important)

This is often ignored.

If inflation is:

- 6% annually

And your return is:

- 10%

Your real return is:

- Around 4%

This means:

Returns must beat inflation to create real wealth.

To understand this deeper, you should read how inflation impacts your mutual fund returns.

Why Many Investors Get Disappointed

Unrealistic Expectations

- Expecting fixed returns

- Expecting high returns every year

Short-Term Thinking

- Evaluating performance too early

Wrong Fund Selection

- Choosing based on past performance

You can avoid this by learning how to choose the right mutual fund in India.

Ignoring Market Cycles

Markets go through ups and downs.

Understanding SIP in bear market vs bull market helps manage expectations.

What Is a Good Return?

Practical Benchmarks

- 6% to 8% → conservative

- 8% to 12% → good

- 12% to 14% → very good

- 15%+ → exceptional (not consistent)

Do not expect consistency every year.

Reality Check Framework (Important Section)

Before expecting returns, ask yourself:

1. What is my investment duration?

- Less than 3 years → lower expectations

- More than 7 years → higher probability

2. What is my risk tolerance?

- Low risk → lower returns

- High risk → higher volatility

3. What is my asset allocation?

- Balanced allocation improves consistency

You can explore this through mutual fund portfolio allocation strategy (equity vs debt vs hybrid).

4. Am I consistent?

- SIP consistency matters more than timing

How to Improve Your Returns

Stay Invested Long Term

- Time reduces volatility

Invest Consistently

- SIP builds discipline

Increase Investment Over Time

- Increase SIP with income

Avoid Emotional Decisions

- Do not panic during market falls

To handle such situations, you should read how to recover from mutual fund losses.

Use Market Corrections Wisely

- Invest more during downturns

You can learn this from how to invest during market crashes in mutual funds.

Common Mistakes to Avoid

Expecting Guaranteed Returns

Mutual funds are market-linked.

Comparing with Fixed Deposits

They serve different purposes.

Frequent Switching

Reduces long-term gains.

Stopping SIP

Breaks compounding.

Ignoring Inflation

Reduces real returns.

Advanced Insight: Consistency Beats High Returns

Successful investors focus on:

- Discipline

- Time in the market

- Consistent investing

Not on:

- Short-term gains

- Market timing

Frequently Asked Questions (FAQs)

Can mutual funds guarantee returns?

No. Returns depend on market performance.

What is a realistic return expectation?

10% to 12% for equity funds over the long term.

Can I get 15% every year?

No. Returns fluctuate.

Are mutual funds better than FD?

They offer higher potential returns but come with risk.

How long should I invest?

At least 5 years, preferably longer.

Which fund type gives the highest returns?

Equity funds, but with higher volatility.

Final Thought

If you want to succeed in mutual fund investing:

Align your expectations with reality.

Mutual funds are not designed for quick profits.

They are designed for:

- Long-term growth

- Wealth creation

- Financial stability

If you stay disciplined and patient:

Your returns will naturally follow over time.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply