By Ashok Prasad, Founder, Niyyam

Published: May 2026

The Financial Question Most Indians Avoid Until It Is Too Late

Introduction

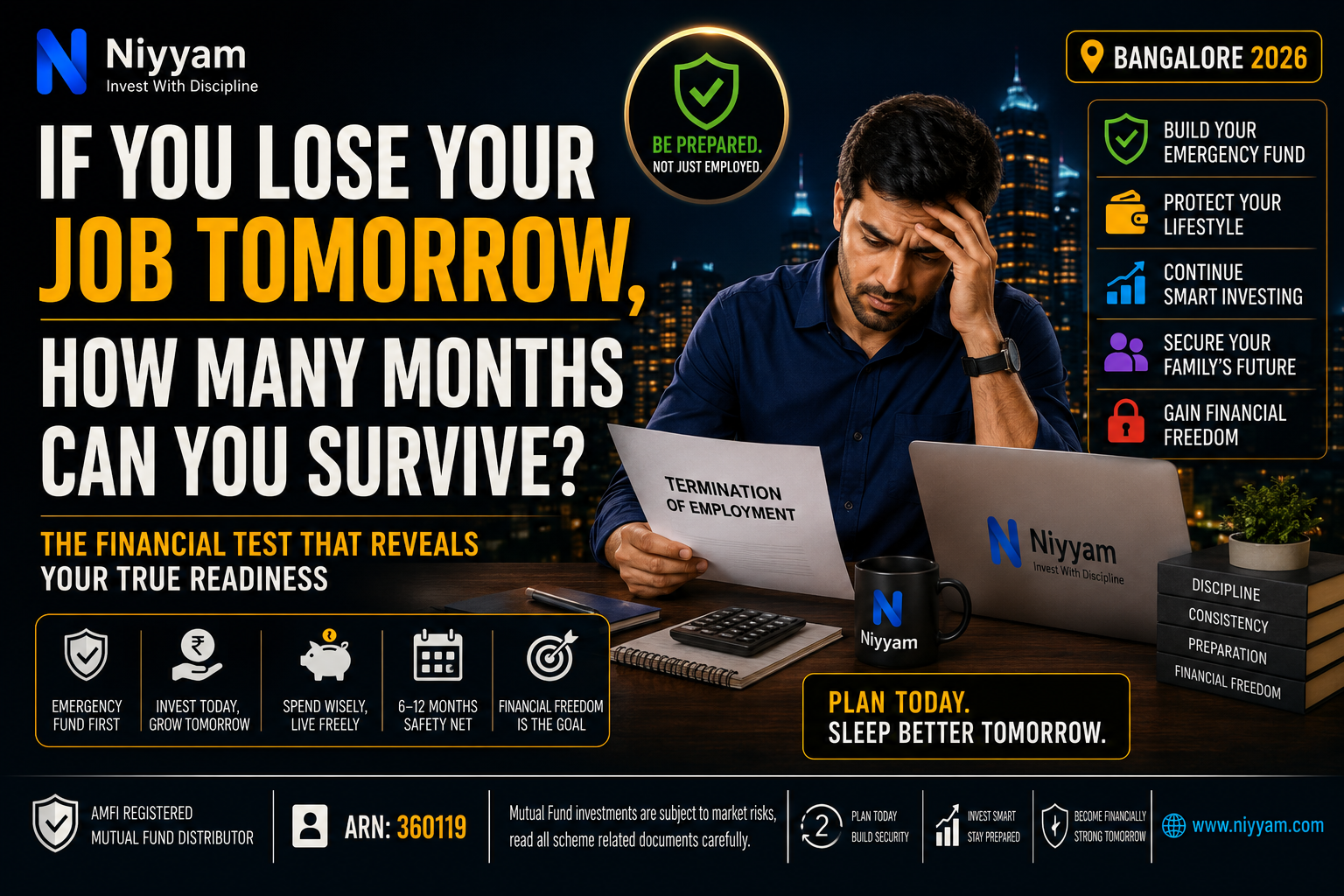

If You Lose Your Job Tomorrow, how many months can you survive without a salary?

Most people never ask themselves this question until they are forced to.

In today’s uncertain economic environment, understanding how long you can survive after losing your job may be one of the most important financial calculations you ever make.

Imagine this.

Tomorrow morning, you wake up as usual.

You check your phone.

You make your coffee.

You get ready for work.

Then an email arrives.

“Important Organizational Update.”

You open it.

Within a few minutes, you discover something that millions of professionals never expect:

Your role has been eliminated.

Your salary stops.

But your life does not.

Your rent is still due.

Your home loan EMI still needs to be paid.

Your car EMI continues.

Your children’s school fees remain payable.

Electricity bills continue arriving.

Medical expenses continue.

Family responsibilities remain exactly the same.

Suddenly, a question that seemed irrelevant yesterday becomes the most important financial question of your life:

If you lose your job tomorrow, how many months can you survive?

One month?

Three months?

Six months?

A year?

Or would you need to borrow money almost immediately?

Most Indians spend years planning:

- Vacations

- Cars

- Homes

- Children’s education

- Retirement

But very few spend time preparing for the possibility that their primary source of income could suddenly disappear.

And that is exactly why this article matters.

💡 Key Takeaways

- Your salary is not your wealth.

- High income does not automatically create financial security.

- The real test of financial strength begins when the salary stops.

- Emergency funds are not optional. They are financial survival tools.

- Lifestyle inflation is one of the biggest reasons high-income professionals remain financially vulnerable.

- Financial freedom begins when your life does not depend on the next salary credit.

Direct Answer

If losing your job tomorrow would force you to borrow money, break investments, delay EMI payments, or depend on family support within a few months, you are financially vulnerable regardless of how much you earn.

A person earning ₹12 lakh annually with:

- An emergency fund

- SIP investments

- Controlled expenses

may be significantly stronger financially than a person earning ₹40 lakh annually with:

- Large EMIs

- Credit card debt

- No emergency fund

- Lifestyle inflation

The most important financial metric is not your salary.

It is your survival period.

Why This Question Matters More Than Ever in 2026

Ten years ago, many professionals believed:

- Good jobs were stable.

- Corporate careers were predictable.

- Technology jobs were secure.

- Large companies provided long-term protection.

Today, the reality looks very different.

Over the last few years, we have seen:

- Startup layoffs

- Technology layoffs

- Hiring freezes

- AI-driven automation

- Global economic slowdowns

- Cost-cutting initiatives

- Corporate restructuring

Thousands of highly qualified professionals have discovered a painful truth:

Your employer owes you a salary. They do not owe you lifetime employment.

This is why every professional should maintain a financial backup plan.

The Salary Illusion

One of the biggest financial myths in India is:

“I earn a high salary, therefore I am financially secure.”

Unfortunately, this assumption is often wrong.

A salary is income.

It is not wealth.

It is not financial freedom.

It is not financial resilience.

Many professionals earning:

- ₹20 lakh annually

- ₹30 lakh annually

- ₹50 lakh annually

- Even ₹1 crore annually

still struggle financially when income stops.

This is exactly the situation discussed in our article:

Salary Rich, Wealth Poor: Why High Income No Longer Guarantees Financial Freedom in India (2026)

Many professionals appear wealthy from the outside.

But their entire lifestyle depends on one thing:

The next salary credit.

Test Case 1: The High Earner

Consider Rahul.

Annual Salary:

₹30 lakh

Monthly Income:

₹2.5 lakh

Monthly Expenses:

- Rent: ₹45,000

- Car EMI: ₹22,000

- Personal loan EMI: ₹12,000

- Credit card bills: ₹18,000

- Household expenses: ₹35,000

- Lifestyle spending: ₹30,000

- Miscellaneous expenses: ₹20,000

Total Monthly Spending:

₹1.82 lakh

Emergency Fund:

₹1 lakh

If Rahul loses his job tomorrow:

Survival Period = Less Than One Month

Despite earning ₹30 lakh annually, Rahul is financially vulnerable.

Why?

Because income is high.

But resilience is low.

Test Case 2: The Disciplined Investor

Now consider Meera.

Annual Salary:

₹12 lakh

Monthly Income:

₹1 lakh

Monthly Expenses:

- Rent: ₹20,000

- Household expenses: ₹20,000

- Insurance: ₹3,000

- Transportation: ₹5,000

- Miscellaneous expenses: ₹7,000

Total Monthly Spending:

₹55,000

Emergency Fund:

₹6 lakh

Monthly SIP:

₹15,000

If Meera loses her job tomorrow:

Survival Period = Almost 11 Months

Who is financially stronger?

The answer surprises many people.

Income does not determine financial strength.

Financial habits do.

The Lifestyle Inflation Trap

One of the biggest reasons people remain financially vulnerable is lifestyle inflation.

As salaries rise, expenses rise too.

People upgrade:

- Apartments

- Cars

- Smartphones

- Vacations

- Restaurants

- Subscriptions

- Shopping habits

None of these are necessarily bad.

The problem begins when expenses grow faster than wealth.

Soon:

- Higher salary creates higher spending.

- Higher spending creates higher obligations.

- Higher obligations create financial dependence.

Eventually, people become trapped.

This is why many professionals earning excellent salaries still feel financially stressed.

In our article:

Why Even ₹30 LPA Salaries Feel Poor in Bangalore in 2026

we explored how:

- Rising rents

- Lifestyle expectations

- Inflation

- Social pressure

are causing many professionals to feel financially insecure despite earning more than ever before.

Income grows.

Expenses grow.

But wealth often does not.

The Bangalore Reality

Few cities illustrate this problem better than Bangalore.

On paper, Bangalore is one of India’s highest-paying job markets.

Thousands of professionals earn:

- ₹15 LPA

- ₹25 LPA

- ₹40 LPA

- ₹60 LPA+

Yet many still experience financial stress.

Why?

Because expenses have increased dramatically.

Today’s professionals face:

- High rents

- Expensive childcare

- Rising healthcare costs

- Increasing insurance premiums

- Growing lifestyle expectations

- Frequent job uncertainty

A professional earning ₹2 lakh per month may still feel financially insecure if:

- ₹50,000 goes toward rent

- ₹30,000 goes toward EMIs

- ₹20,000 goes toward insurance and utilities

- ₹25,000 goes toward lifestyle spending

- ₹20,000 goes toward family obligations

The issue is not income.

The issue is preparation.

High income can mask financial weakness.

How Much Emergency Fund Do You Actually Need?

One of the biggest mistakes people make is underestimating how long it may take to find another job.

Many assume:

- “I’ll get another offer in a month.”

- “My experience is strong.”

- “The market will recover.”

Sometimes that happens.

Sometimes it doesn’t.

A practical framework is:

Minimum Protection

3 Months of Expenses

Suitable only if:

- You have exceptional job security

- You work in a highly employable field

- You have no dependents

Recommended Protection

6 Months of Expenses

Suitable for most salaried professionals.

This is the minimum target many financial planners recommend.

Strong Financial Protection

12 Months of Expenses

Particularly useful for:

- Startup employees

- Consultants

- Freelancers

- Business owners

- Single-income families

- Professionals in volatile industries

The more uncertain your income, the larger your emergency fund should be.

How To Calculate Your Survival Period

Most people know their salary.

Very few know their survival period.

The calculation is simple:

Survival Period Formula

Emergency Fund ÷ Monthly Essential Expenses

Example:

Emergency Fund:

₹6,00,000

Monthly Essential Expenses:

₹60,000

Result:

₹6,00,000 ÷ ₹60,000 = 10 Months

This means you can survive for approximately ten months without earning additional income.

Now ask yourself:

Do you know your number?

Because that number is often more important than your annual salary.

Emergency Fund vs SIP Investments

Many investors ask:

“Should I stop my SIPs and build an emergency fund first?”

The answer depends on your current financial position.

If you have:

- No emergency fund

- Significant liabilities

- Family responsibilities

- Dependents relying on your income

then building an emergency reserve should become a priority.

However, that does not mean long-term investing becomes unimportant.

As discussed in:

Can SIP Really Make an Ordinary Salaried Person a Crorepati?

wealth creation requires:

- Consistency

- Discipline

- Time

- Patience

Think of it this way:

Emergency Fund

Protects your present.

SIP Investments

Build your future.

You need both.

Not one instead of the other.

Visual Asset: Where Should Your Monthly Income Go?

You can convert this section into a graphic inside the blog.

Monthly Salary

│

▼

Essential Expenses

(Rent, EMI, Utilities, Food)

│

▼

Emergency Fund

(6–12 Months Reserve)

│

▼

SIP Investments

(Long-Term Wealth Creation)

│

▼

Financial FreedomEmergency Funds Protect Your Present.

SIP Investments Build Your Future.

You Need Both.

Quick Self-Test: How Financially Prepared Are You?

Answer these questions honestly.

□ Could I pay my rent or EMI for the next 6 months without a salary?

□ Could I support my family if my income stopped tomorrow?

□ Do I know exactly how much I spend every month?

□ Do I have at least six months of expenses available in liquid form?

□ Would I need to break long-term investments if I lost my job?

□ Would I need financial help from family or friends?

□ Could I comfortably search for another job without panic?

□ Do I have adequate health insurance and emergency savings?

Scoring Yourself

7–8 YES Answers

You are financially well prepared.

4–6 YES Answers

You are reasonably prepared, but there is room for improvement.

0–3 YES Answers

Your financial resilience may need immediate attention.

The best time to build an emergency fund is before you need it.

Not after.

The Emotional Cost of Job Loss

Most people focus on money.

Very few talk about emotions.

Job loss can trigger:

- Anxiety

- Stress

- Fear

- Self-doubt

- Relationship pressure

- Family tension

- Loss of confidence

Financial preparation cannot eliminate these feelings completely.

But it can reduce them dramatically.

Imagine two people:

Person A loses their job with ₹50,000 in savings.

Person B loses their job with ₹8 lakh in savings.

Who sleeps better that night?

Who can make better decisions?

Who can search for opportunities calmly?

The answer is obvious.

Money does not buy happiness.

But financial preparedness can reduce unnecessary panic.

Startup Layoffs and Financial Reality

Many professionals continue believing:

“I’ll prepare later.”

Unfortunately:

- Layoffs do not provide advance notice.

- Economic slowdowns do not ask permission.

- AI disruption does not wait for people to become ready.

This is exactly why we discussed in:

Startup Layoffs in Bangalore: Why Every IT Employee Needs a Financial Backup Plan

that financial resilience should be built before uncertainty arrives.

Hope is not a financial strategy.

Preparation is.

What Financial Freedom Really Means

Many people misunderstand financial freedom.

When asked what financial freedom looks like, common answers include:

- A luxury car

- A large home

- International vacations

- Business class travel

- A high-paying job

- A seven-figure salary

While these things may be enjoyable, they are not the true definition of financial freedom.

The real definition is much simpler.

Financial freedom begins when your survival does not depend on the next salary credit.

That is the point where money starts working for you instead of you constantly working for money.

This idea is closely related to the concepts discussed in:

How Much Should Bangalore Techies Invest Monthly to Retire Before 45?

The ultimate objective is not simply earning more.

The objective is gradually reducing your dependence on active income.

Because the day your expenses can survive without your salary is the day you begin moving toward true financial freedom.

A Practical Action Plan

If this article made you uncomfortable, that is not necessarily a bad thing.

Sometimes discomfort highlights areas that need attention.

Instead of worrying about uncertainty, focus on preparation.

Step 1: Calculate Your Monthly Essential Expenses

Include only necessities:

- Rent or home loan EMI

- Utilities

- Insurance premiums

- Groceries

- Transportation

- Children’s education

- Essential family expenses

Ignore:

- Vacations

- Shopping

- Luxury spending

- Entertainment

Your emergency fund should be based on essentials, not lifestyle spending.

Step 2: Calculate Your Survival Period

Use the formula discussed earlier:

Emergency Fund ÷ Monthly Essential Expenses

Write down the number.

Do not guess.

Know it.

Step 3: Build an Emergency Fund

Aim for:

Minimum Target

- 6 Months of Expenses

Preferred Target

- 12 Months of Expenses

Especially if you work in:

- Technology

- Startups

- Consulting

- Freelancing

- Entrepreneurship

Step 4: Continue SIP Investments

Emergency funds protect you.

SIPs grow your wealth.

long-term wealth creation is usually the result of:

- Consistency

- Discipline

- Time

- Patience

Not market timing.

Not speculation.

Not luck.

Step 5: Avoid Lifestyle Inflation

Every salary increase creates a choice:

Option A

Increase expenses.

Option B

Increase wealth.

Most people choose Option A.

Financially successful people often choose Option B.

Step 6: Review Your Financial Position Annually

Ask yourself:

- Has my emergency fund increased?

- Have my investments increased?

- Has my dependence on salary decreased?

- Am I financially stronger than I was last year?

If the answer is yes, you are moving in the right direction.

The Question That Reveals Your True Financial Health

People often ask:

“What is my net worth?”

“Which mutual fund should I invest in?”

“How much should I save?”

These are important questions.

But there is one question that may reveal more about your financial health than all of them combined:

If you lose your job tomorrow, how many months can you survive?

Because that answer reflects:

- Your savings habits

- Your spending habits

- Your financial discipline

- Your preparedness

- Your resilience

More than your salary ever can.

Final Thoughts

Nobody plans to lose a job.

Nobody expects a layoff.

Nobody anticipates economic uncertainty.

Yet every year, thousands of professionals face unexpected financial disruption.

The difference between panic and stability often comes down to a single factor:

Preparation.

A large salary can disappear.

A prestigious job title can disappear.

A booming industry can slow down.

But disciplined financial habits remain.

Your emergency fund remains.

Your investments remain.

Your preparation remains.

And when uncertainty arrives, those things matter far more than your annual income.

So before you close this article, take a moment and answer one final question honestly:

If you lose your job tomorrow, how many months can you survive?

If the answer makes you uncomfortable, today may be the perfect day to start building a stronger financial future.

Frequently Asked Questions (FAQs)

How much emergency fund should a salaried employee maintain?

Most financial planners recommend maintaining between 6 and 12 months of essential expenses, depending on income stability, family responsibilities, and career risk.

Should emergency funds be invested in equity mutual funds?

Generally, no.

Emergency funds are designed to provide:

- Immediate accessibility

- Capital preservation

- Liquidity during emergencies

- Financial stability during uncertain periods

Equity mutual funds can experience significant short-term volatility and may not be suitable for money that might be needed urgently.

Common places investors consider for emergency funds include:

- Savings Accounts

- Fixed Deposits

- Liquid Mutual Funds

- Arbitrage Funds (depending on liquidity requirements, tax considerations, and risk tolerance)

The most suitable option depends on:

- Liquidity needs

- Financial goals

- Risk appetite

- Tax considerations

Accessibility First. Returns Second.

The primary purpose of an emergency fund is not maximizing returns.

It is ensuring money is available when it is needed the most.

Can SIP investments replace an emergency fund?

No.

SIP investments and emergency funds serve completely different purposes.

Emergency Fund

Protects your short-term financial stability.

SIP Investments

Build long-term wealth.

Both are important.

What is the biggest financial mistake after receiving a salary hike?

Allowing lifestyle inflation to grow faster than savings and investments.

A higher salary should ideally improve financial resilience, not simply increase spending.

Is a high salary enough to guarantee financial security?

No.

Financial security depends on:

- Savings

- Investments

- Emergency preparedness

- Financial discipline

- Controlled spending

Not income alone.

Disclaimer

This article is intended solely for educational and informational purposes and should not be considered investment, tax, legal, or financial advice.

Mutual fund investments are subject to market risks. Investors should evaluate their individual financial goals, liquidity requirements, risk tolerance, and consult qualified financial professionals before making investment decisions.

Niyyam does not guarantee returns, investment performance, or financial outcomes.

Niyyam.com is operated by Tech Margon Wealth Private Limited.

AMFI Registered Mutual Fund Distributor

ARN: 360119