By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

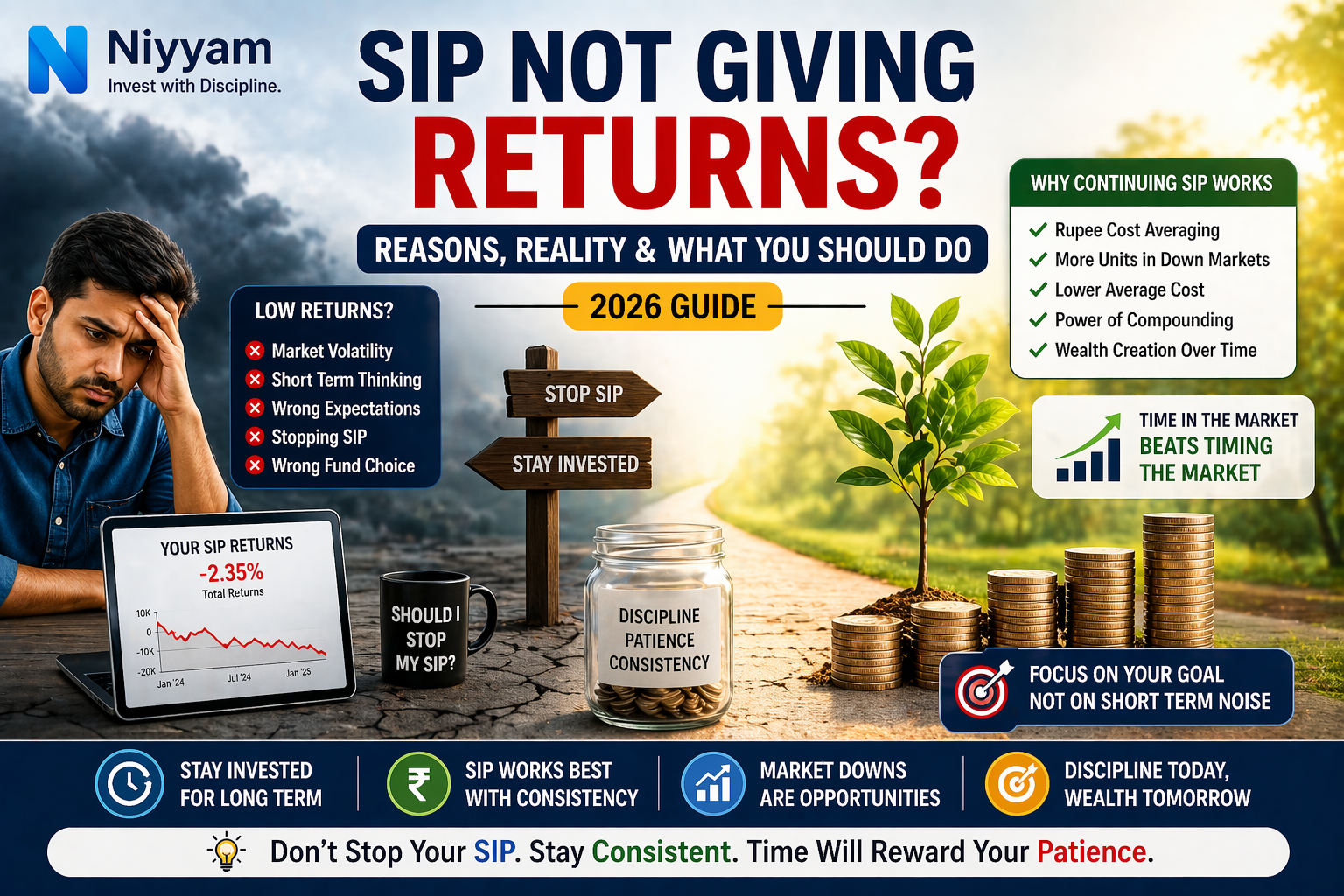

SIP not giving returns is one of the most common concerns among mutual fund investors.

You start a SIP expecting steady growth. But after months—or even a few years—you check your portfolio and see:

- Low returns

- Flat performance

- Or even negative returns

This creates frustration and doubt.

Many investors react emotionally:

- Stop their SIP

- Withdraw investments

- Shift to low-risk options

But here is the truth:

In most cases, the problem is not your SIP—it is your expectations, time horizon, or strategy.

Understanding what is happening inside your investment is the key to making the right decision.

💡 Key Takeaways

- SIP returns depend on time, market cycles, and fund selection

- Short-term underperformance is normal in equity investing

- Stopping SIP during low-return phases destroys compounding

- Market corrections actually benefit SIP investors

- Reviewing strategy is better than reacting emotionally

- Consistency is the biggest driver of SIP success

Direct Answer

SIP may not give returns in the short term due to market volatility and timing, but consistent investing over the long term typically leads to strong wealth creation through compounding.

If you are new, start with

What is a Mutual Fund and How It Works (Beginner Guide)

to understand the basics.

Why SIP Is Not Giving Returns

1. Investment Duration Is Too Short

SIP is not a short-term tool.

| Duration | Behavior |

|---|---|

| 0–3 years | High volatility |

| 3–5 years | Stabilization |

| 7–10 years | Strong compounding |

If your SIP is less than 3 years old, low or negative returns are normal.

To understand this, refer to

How SIP Builds Wealth Through Compounding

2. Market Cycle Impact (Expanded Insight)

Markets do not move in a straight line.

They go through:

- Bull phases (rising markets)

- Bear phases (falling markets)

- Sideways phases (flat markets)

If your SIP started during a peak:

- Initial returns may look poor

- Your portfolio may appear stagnant

Deeper Insight

This phase is actually beneficial.

Because:

- You buy more units at lower prices

- Your average cost reduces

3. Wrong Fund Selection

Sometimes the issue lies in the fund itself.

Common mistakes:

- Choosing underperforming funds

- Selecting the wrong category

- Not aligning with goals

To avoid this, refer to

How to Choose the Right Mutual Fund in India

4. Unrealistic Expectations

Many investors expect:

- Fixed returns

- High returns every year

But equity investing is not linear.

To understand reality, refer to

How Much Return Can You Expect from Mutual Funds in India?

5. Poor Asset Allocation

An unbalanced portfolio leads to:

- Excess volatility (too much equity)

- Limited growth (too much debt)

A proper mix is essential.

To understand this, refer to

How to Build a Mutual Fund Portfolio for Long-Term Wealth Creation

What Is Actually Happening During Low Returns

During market corrections:

- Prices fall

- Your SIP buys more units

- Your average cost reduces

This is called rupee cost averaging.

Why This Matters

- You accumulate more units

- Future returns improve significantly

To understand this, refer to

What Is Rupee Cost Averaging in SIP and How It Works

What Happens in First 3 Years vs 10–15 Years

First 3 Years

- Volatile returns

- Low visibility of growth

- High uncertainty

10–15 Years

- Compounding accelerates

- Growth becomes exponential

- Wealth multiplies

Key Insight

Most wealth is created in later years, not early years.

What Happens If You Stop SIP vs Continue?

Scenario

- SIP: ₹10,000/month

- Duration: 3 years

If You Stop

- Lock in low returns

- Miss future growth

- Lose compounding

If You Continue

- Benefit from recovery

- Improve average cost

- Build long-term wealth

Insight

Continuing SIP is usually the better decision.

Action Framework: What You Should Do

Step 1: Do Not Panic

Avoid emotional decisions.

Step 2: Check Your Investment Horizon

Ask:

Have I invested for at least 5 years?

If not:

Continue your SIP.

Step 3: Evaluate Fund Performance

Check:

- 3–5 year track record

- Performance vs benchmark

- Fund strategy

Step 4: Continue SIP

Consistency drives results.

Step 5: Increase SIP During Market Falls

If possible:

- Invest more during corrections

This helps:

- Lower cost

- Increase returns

Step 6: Rebalance Portfolio

Over time:

- Allocation changes

Review and adjust periodically.

To understand this, refer to

How to Rebalance Your Mutual Fund Portfolio

Real-Life Case Studies (Expanded)

Case Study 1: Short-Term Investor

- SIP: ₹10,000/month

- Duration: 2 years

Outcome

- Low returns

Reality

- More units accumulated

- Future potential improved

Case Study 2: Medium-Term Investor

- SIP: ₹15,000/month

- Duration: 6 years

Outcome

- Stable returns

- Visible compounding

Case Study 3: Long-Term Investor

- SIP: ₹10,000/month

- Duration: 12 years

Outcome

- Significant wealth creation

- Exponential growth

Case Study 4: Investor Who Stopped SIP

- SIP stopped after 2 years

Outcome

- Missed recovery

- Lower returns

Insight

Stopping SIP destroys long-term potential.

When Should You Take Action?

You should review your SIP if:

- Fund underperforms for 3+ years

- Fund strategy changes

- Your financial goals change

When Should You NOT Take Action?

Do not react if:

- Market is temporarily down

- Returns are low in short term

- SIP duration is less than 3–5 years

Common Mistakes to Avoid

- Expecting quick returns

- Checking portfolio too frequently

- Stopping SIP during market fall

- Chasing past performance

- Ignoring long-term strategy

To build confidence, refer to

How to Invest During Market Crashes in Mutual Funds

Advanced Insight: Why SIP Works Even When Returns Look Low

Even when returns appear weak:

- You accumulate more units

- Average cost reduces

- Future gains improve

Key Insight

SIP works best when it feels like it is not working.

Behavioral Reality: Why Investors Fail

Investors do not fail because SIP does not work.

They fail because:

- They lack patience

- They react emotionally

- They exit early

Insight

Behavior matters more than strategy.

How Long Should You Continue SIP?

| Duration | Outcome |

|---|---|

| < 3 years | Uncertain |

| 5 years | Stable |

| 10+ years | Strong wealth creation |

Frequently Asked Questions (FAQs)

Why is my SIP showing negative returns?

Due to short-term market volatility.

Should I stop SIP if returns are low?

No, continuing SIP is usually better.

When should I review SIP?

Every 6–12 months.

Can SIP guarantee returns?

No, returns are market-linked.

Should I switch funds?

Only if performance is consistently poor.

How long should I stay invested?

At least 5 years, preferably longer.

Conclusion

If your SIP is not giving returns, the answer is not panic—it is patience.

Final Thought

SIP is not a shortcut.

It is a disciplined process.

Low-return phases are not failures.

They are opportunities.

If you stay consistent:

Your long-term wealth will follow.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.