By Ashok Prasad, Founder, Niyyam

Published: March 2026

Introduction

SIP vs RD is one of the most common questions among investors starting their financial journey.

Both options look similar on the surface:

- You invest a fixed amount every month

- You build savings over time

- You develop financial discipline

But the similarity ends there.

The way they generate returns, handle risk, and build wealth is fundamentally different.

Most beginners choose between SIP and RD without fully understanding these differences.

As a result, they often:

- Use RD for long-term goals (which limit wealth)

- Avoid SIP due to fear of market fluctuations

If you want to make the right decision, you must understand how each option actually works.

💡 Key Takeaways

- SIP offers higher return potential (10–12%)

- RD provides fixed and predictable returns (5–7%)

- SIP is market-linked and volatile in the short term

- RD is safe and stable

- SIP can beat inflation

- RD often fails to generate real returns after inflation

- SIP is more tax-efficient

- Both can be used together for a balanced strategy

Direct Answer

SIP is better for long-term wealth creation, while RD is better for short-term savings and guaranteed returns.

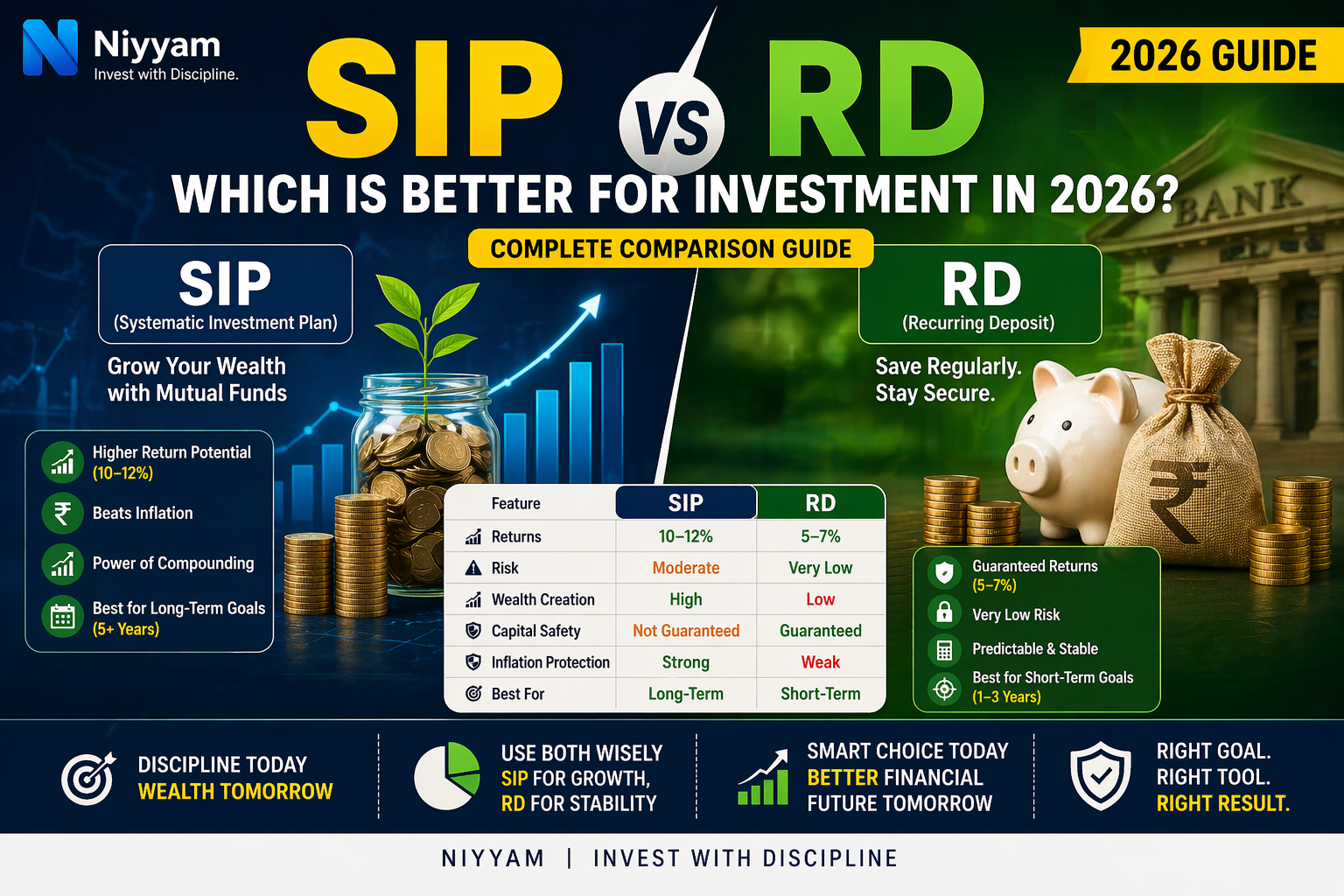

SIP vs RD – Quick Comparison

| Feature | SIP | RD |

|---|---|---|

| Returns | Market-linked (10–12%) | Fixed (5–7%) |

| Risk | Moderate | Very low |

| Wealth Creation | High | Low |

| Capital Safety | Not guaranteed | Guaranteed |

| Inflation Protection | Strong | Weak |

| Best For | Long-term goals | Short-term savings |

Understanding SIP (How It Actually Works)

SIP (Systematic Investment Plan) is an investment method where you invest regularly in mutual funds.

But here is what many people do not understand:

You are not just depositing money.

You are buying units of a mutual fund.

How SIP Works

- Each month, your money buys units based on NAV

- When markets fall → you get more units

- When markets rise → value of units increases

This is called rupee cost averaging.

Key Benefits

- Compounding effect

- Market participation

- Long-term wealth creation

To understand long-term wealth building, refer to

Can SIP Make You Crorepati? Real Numbers, Time & Strategy (2026 Guide)

Understanding RD (How It Actually Works)

Recurring Deposit (RD) is a savings product offered by banks.

You deposit a fixed amount every month and earn a fixed interest rate.

How RD Works

- Fixed monthly contribution

- Fixed interest rate (5–7%)

- Interest compounded quarterly

Key Characteristics

- Predictable returns

- No market exposure

- Low risk

But here is the limitation:

Growth is linear, not exponential.

Returns Comparison: SIP vs RD (Reality Check)

10-Year Example

| Investment Type | Monthly Investment | Total Invested | Final Value |

|---|---|---|---|

| SIP (12%) | ₹10,000 | ₹12 lakh | ~₹23–24 lakh |

| RD (6.5%) | ₹10,000 | ₹12 lakh | ~₹16–17 lakh |

20-Year Example

| Investment Type | Monthly Investment | Total Invested | Final Value |

|---|---|---|---|

| SIP (12%) | ₹10,000 | ₹24 lakh | ~₹1 crore |

| RD (6.5%) | ₹10,000 | ₹24 lakh | ~₹45–50 lakh |

Key Insight

The difference is not small.

It is massive.

SIP creates wealth.

RD builds savings.

The Power of Compounding (Why SIP Wins Long-Term)

Compounding means your returns generate additional returns.

In SIP:

- Returns are reinvested

- Growth accelerates over time

- Wealth multiplies

In RD:

- Returns are fixed

- Growth is predictable but slow

To understand how increasing SIP improves compounding, refer to

Step-Up SIP Strategy: How to Increase SIP and Build 2–3x More Wealth (2026 Guide)

Risk Comparison (What You Must Understand)

| Factor | SIP | RD |

|---|---|---|

| Market Risk | Yes | No |

| Capital Safety | Not guaranteed | Guaranteed |

| Volatility | High (short-term) | None |

Key Insight

SIP risk is temporary (market-driven)

RD safety is permanent but limited in growth

When SIP Feels “Not Working” (Short-Term Reality)

Many investors quit SIP early.

Why?

Because:

- Markets fall

- Returns look low

- Portfolio shows negative returns

This is normal.

SIP performance depends on time.

Short-term returns can be volatile.

Long-term returns are more stable and rewarding.

To understand this behavior, refer to

Why Most SIP Investors Fail to Build Wealth

Inflation Impact (The Most Ignored Factor)

Inflation silently reduces your purchasing power.

Comparison

| Factor | SIP | RD |

|---|---|---|

| Inflation Beating Ability | High | Low |

| Real Returns | Positive | Often negligible |

Example

If inflation is 6%:

- RD return (6.5%) → real return ~0.5%

- SIP return (12%) → real return ~6%

Insight

RD may not grow your money meaningfully after inflation.

Taxation Comparison

| Factor | SIP | RD |

|---|---|---|

| Tax Type | Capital gains | Interest income |

| Tax Efficiency | Higher | Lower |

| Tax Impact | Moderate | High |

Key Insight

RD interest is taxed every year as per your income slab.

SIP (especially equity funds) is more tax-efficient over the long term.

Behavioral Reality: Why People Prefer RD

Despite lower returns, many people prefer RD.

Reasons

- Fear of market fluctuations

- Desire for certainty

- Lack of financial knowledge

- Short-term mindset

Insight

RD feels safe.

SIP builds wealth.

Real-Life Scenario (Clear Understanding)

Investor A (SIP)

- Invests ₹10,000/month

- Duration: 20 years

- Outcome: ₹1 crore+

Investor B (RD)

- Invests ₹10,000/month

- Duration: 20 years

- Outcome: ₹45–50 lakh

Key Insight

Same discipline.

Different instrument.

Very different financial future.

Who Should Choose SIP vs RD?

Choose SIP if:

- You want long-term wealth creation

- You can stay invested for 5–20 years

- You can tolerate short-term volatility

Choose RD if:

- You want guaranteed returns

- You have short-term goals (1–3 years)

- You prefer stability over growth

Balanced Strategy: SIP + RD (Best Approach)

The smartest investors do not choose one.

They use both.

Suggested Allocation

| Investment | Purpose |

|---|---|

| SIP (60–80%) | Growth |

| RD (20–40%) | Stability |

Insight

SIP builds wealth.

RD provides safety.

Common Mistakes to Avoid

- Using RD for long-term wealth goals

- Avoiding SIP due to fear

- Ignoring inflation

- Expecting SIP to be risk-free

To identify weak investments, refer to

How to Identify a Bad Mutual Fund? Warning Signs Investors Must Know

Decision Framework (Most Important Section)

| If You Want | Choose |

|---|---|

| High returns | SIP |

| Capital safety | RD |

| Long-term wealth | SIP |

| Short-term savings | RD |

| Inflation protection | SIP |

Frequently Asked Questions (FAQs)

Which is better, SIP or RD in India?

SIP is better for long-term wealth creation, RD for short-term safety.

Can RD beat SIP returns?

No, RD cannot outperform SIP in the long term.

Is SIP risky?

Yes, in the short term. But it becomes more stable over long periods.

Should I invest in SIP or RD?

Choose based on your goals and time horizon.

Conclusion

SIP and RD are not competing products.

They serve different purposes.

Final Verdict

- SIP = Wealth creation

- RD = Capital protection

Final Thought

Smart investing is not about choosing one option.

It is about using the right tool for the right goal.

If used correctly:

You can achieve both growth and financial security.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply