By Ashok Prasad, Founder, Niyyam

Published: March 2026

When it comes to investing, one question matters more than fund selection:

“How should I allocate my investments?”

Many investors focus on choosing the “best mutual fund,” but ignore the most important factor:

Asset allocation.

💡 Key Takeaways

- The Age-Equity Rule: Use the “100-Minus-Age” rule as a starting point to determine your equity exposure (e.g., at age 30, keep roughly 70% in equity).

- Aggressive Growth (20s-30s): Maximize wealth by focusing on high-growth equity funds since your time horizon allows you to ride out market volatility.

- Preservation Mode (40s-50s): Gradually shift a portion of your gains into Debt and Hybrid funds to protect your capital as you approach retirement.

- Holistic Planning: Asset allocation isn’t just about age; it should also account for your immediate liquidity needs and emergency fund requirements.

Because in reality:

Your returns are driven more by how you allocate your money than where you invest it.

In this guide, you will learn:

- What asset allocation means

- Why should it change with age

- How to allocate in your 20s, 30s, 40s, and 50+

- A practical framework for Indian investors in 2026

What is Asset Allocation?

Asset allocation means how you divide your money across different asset classes, such as:

- Equity (mutual funds, stocks)

- Debt (bonds, debt funds, fixed income)

- Cash or liquid investments

Simple Understanding:

- Equity = Growth

- Debt = Stability

- Cash = Liquidity

Why Asset Allocation is Critical

Many investors make this mistake:

- They chase returns

- They invest randomly

- They ignore balance

But in reality:

- Wrong allocation can destroy returns

- Right allocation can reduce risk and improve outcomes

Important Insight:

- Asset allocation matters more than selecting the best fund

- It determines both risk and return

To understand this better, refer to:

Mutual Fund Portfolio Allocation Strategy (Equity vs Debt vs Hybrid – 2026 Guide)

Why Asset Allocation Should Change With Age

Your financial life evolves.

- Income changes

- Responsibilities increase

- Risk tolerance decreases

Core Principle:

- Younger investors can take more risk

- Older investors need more stability

Because:

- Younger investors have time to recover losses

- Older investors need capital protection

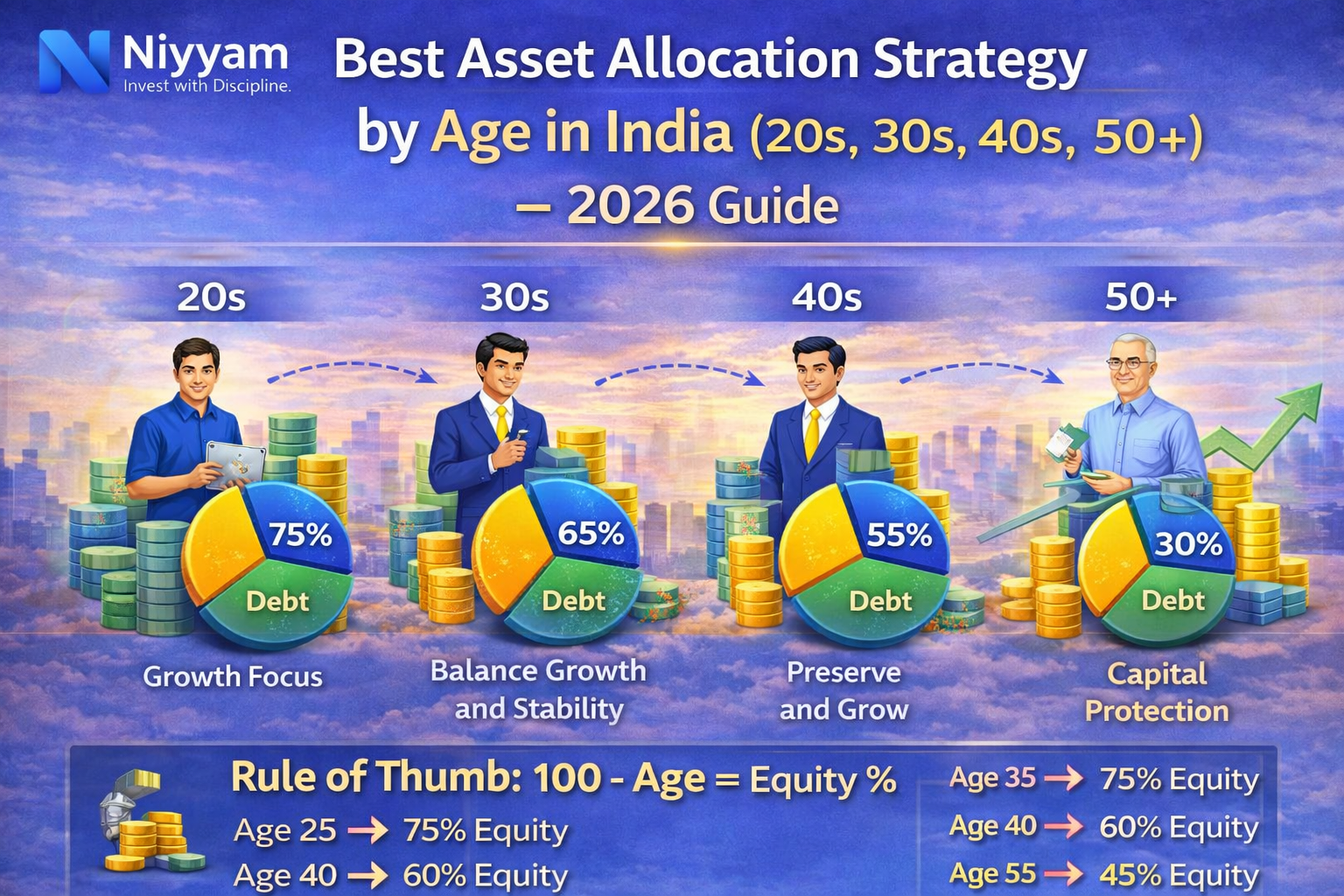

Asset Allocation by Age (2026 Framework)

Let’s break it down practically.

In Your 20s (Age 20–29)

Situation:

- Early career

- Low financial responsibilities

- Long investment horizon

Recommended Allocation:

- 70% – 80% Equity

- 20% – 30% Debt

Why This Works:

- Maximum time for compounding

- Ability to handle volatility

- Higher growth potential

Suggested Funds:

- Index funds

- Large-cap funds

- Mid-cap funds

Key Focus:

- Growth over stability

- Start early and stay consistent

Refer:

How SIP Builds Wealth Through Compounding (With Simple Examples)

In Your 30s (Age 30–39)

Situation:

- Stable income

- Increasing responsibilities

- Long-term goals like home, family

Recommended Allocation:

- 60% – 70% Equity

- 30% – 40% Debt

Why This Works:

- Balance between growth and stability

- Protect against market volatility

- Continue wealth creation

Suggested Funds:

- Large-cap funds

- Index funds

- Hybrid funds

Key Focus:

- Balance growth with risk control

In Your 40s (Age 40–49)

Situation:

- Peak earning years

- High responsibilities (children, loans)

- Medium investment horizon

Recommended Allocation:

- 50% – 60% Equity

- 40% – 50% Debt

Why This Works:

- Reduce volatility

- Protect accumulated wealth

- Maintain moderate growth

Suggested Funds:

- Large-cap funds

- Hybrid funds

- Debt funds

Key Focus:

- Preserve wealth while continuing growth

In Your 50s and Above

Situation:

- Approaching retirement

- Low risk tolerance

- Focus on income and stability

Recommended Allocation:

- 20% – 40% Equity

- 60% – 80% Debt

Why This Works:

- Protect capital

- Reduce market risk

- Ensure stable income

Suggested Funds:

- Debt funds

- Conservative hybrid funds

Key Focus:

- Capital protection and income stability

Quick Allocation Rule of Thumb

A simple way to remember:

- Age-based formula: 100 – Age = Equity Allocation

Example:

- Age 25 → 75% equity

- Age 40 → 60% equity

- Age 55 → 45% equity

Important Note:

- This is a guideline, not a fixed rule

- Adjust based on your risk tolerance

Role of Risk Profile

Age is important, but not the only factor.

Two people of the same age may have:

- Different income levels

- Different financial goals

- Different risk tolerance

Important Insight:

- Risk profile should refine your allocation

- Not everyone should follow the same formula

Refer:

How to Select Mutual Funds Based on Risk Profile in India (Beginner to Advanced Guide 2026)

How Inflation Affects Allocation

Inflation reduces purchasing power.

If your allocation is too conservative:

- Returns may not beat inflation

Key Insight:

- Equity is necessary for long-term inflation-beating returns

Refer:

How Inflation Impacts Your Mutual Fund Returns (And How to Beat It in 2026)

Active vs Passive Role in Allocation

Within equity allocation, you can choose:

- Active funds for higher return potential

- Passive funds for low cost and consistency

Best Approach:

- Combine both for a better balance

Refer:

Active vs Passive Investing in India: Which Strategy Wins in the Long Run? (2026 Guide)

Common Mistakes in Asset Allocation

Ignoring Allocation Completely

- Investing randomly

- No structure

Too Much Equity at Older Age

- High risk

- Large losses near retirement

Too Much Debt at a Younger Age

- Low returns

- Missed growth opportunities

Not Rebalancing Portfolio

- Allocation shifts over time

- Risk increases unintentionally

When Should You Rebalance?

Rebalancing means adjusting your portfolio back to the target allocation.

When to Rebalance:

- Once every year

- When allocation changes significantly

- After major life events

Refer:

How to Rebalance Your Mutual Fund Portfolio (When, Why & How – 2026 Guide)

Real-Life Example

Consider two investors:

Investor A

- Same allocation for the entire life

- No adjustments

Investor B

- Adjusts allocation with age

- Reduces risk gradually

Result:

- Investor A faces a high risk in later years

- Investor B maintains stability and growth

The difference is not returns.

The difference is strategy.

Key Takeaways

- Asset allocation is more important than fund selection

- Allocation should change with age

- Younger investors should focus on growth

- Older investors should focus on stability

- Equity is essential for beating inflation

- Rebalancing is necessary to maintain balance

Final Thought

Investing is not just about choosing funds.

It is about structuring your money wisely.

Your age, goals, and risk tolerance should guide your decisions.

A well-allocated portfolio is the foundation of long-term wealth.

Frequently Asked Questions (FAQs)

1. Is age-based allocation enough?

No. Risk profile and goals also matter.

2. Should I reduce equity with age?

Yes, gradually to reduce risk.

3. Can I keep high equity after 40?

Yes, if your risk tolerance allows it.

4. How often should I rebalance?

At least once a year.

Disclaimer

This content is for educational purposes only and does not constitute investment advice.

Mutual fund investments are subject to market risks. Investors should read all scheme-related documents carefully before investing and consider their financial goals, risk tolerance, and investment horizon.

Share this guide with your friends, family, and colleagues to help them make better financial decisions.

If this article helped you, share it with at least one person who needs this guidance.

Leave a Reply